An Analysis of Environmental Accounting and Firm Profitability of Reliance Industry Limited

Abstract:

Environmental accounting is the ability to provide accurate information in the financial statements regarding the estimated social cost occasioned by the production externalities on the environment and how much deliberate intervention cost had been incurred to bridge the gap between the marginal social cost and the marginal private cost by a firm. The objective of this study is to establish whether there is any significant relationship between environmental accounting and profitability of Reliance Industry Limited, Gujarat. The data for the study were collected from annual reports and accounts of Reliance Industry Limited, Gujarat. The data were analyzed using multiple regression models. The key findings of the study shows that there is significant negative relationship between Environmental Accounting and Return on Capital Employed (ROCE) and Earnings per Share (EPS) and a significant positive relationship between Environmental Accounting and Net Profit Margin and Dividend per Share. Based on this it was recommended that government should give tax credit to organizations that comply with its environmental laws and that environmental reporting should be made compulsory in India so as to improve the performance of organizations and the nation as a whole.

Introduction:

Accounting for environment helps in accurate assessment of costs and benefits of environmental preservation measures of companies. It provides a common framework for organizations to identify and account for past, present and future environmental costs to support managerial decision-making, control and public disclosure. The severity of environmental problems as a global phenomenon has its adverse on the quality of our life. Measures are being taken both at the national and international level to reduce, prevent and mitigate its impact on social, economic and political spheres. The emergence of corporate environmental reporting (CER) in India has been an important development, both for better environmental management and overall corporate governance. Global awareness of stakeholders on corporate environmental performance has already made traditional reporting redundant. Corporate houses run into the risk of loss of faith of their stakeholders, if in future, environmental performance information is not included in their main stream reporting.

Simple adherence to mandatory environmental reporting is insufficient to meet the environmental disclosure expectation of stakeholders. Mandatory reporting is nothing but a minimum prescribed reporting requirement. Companies around the world aspire consciously for improved transparency in disclosure as their core competence. Environmental disclosure through internet would be the future of scientific reporting. A number of recent national and international surveys have identified increase in growth of companies reporting on internet.

2. Environmental Accounting Meaning:

Environmental accounting means a flexible tool to provide information not necessarily provided in traditional managerial systems. Environmental accounting that provides information on performance evaluation of control decision-making and reporting to help managers the economic and environmental implications as well built as the market value of those uses that are not, its use requires a change in culture. Environmental accounting, part of wider changes in the organization and the community it provides and by providing more fundamental knowledge of and participation in everyday work activities, to the continual development of the approach environmental accounting branch of accounting that collect environmental costs and use data in the calculation of cost of goods and services deals. The accounting environment can include activities such as accounting systems that enhance the ability to detect Recording and reporting the work of destruction and environmental pollution and environmental-based integration as a source of CapitaLand consideration of environmental costs as an acceptable cost of computational processes and economic.

3. Environmental accounting in India:

Environmental reporting of Indian companies can be broadly categorized into two types’ mandatory disclosure and voluntary disclosure. Preliminary investigation of this study shows that Indian companies practice more of voluntary environmental reporting in the form of satellite reporting, sustainability reporting, GRI reporting and internet reporting. In year 2001, a country wide survey, the first of its kind, was carried out by Business Today, a business magazine, and The Energy Research Institute (TERI, 2001) to understand the environmental practices of corporate India. Findings of the survey revealed that more than 75% of the sample had environmental policy; about 70% have environmental audit system; 60% had an environment department; four out of every ten Indian Companies had formal environment certification.

As per Indian Constitution, Article 51A of Directive Principles “It shall be the duty of every citizen of India, to protect and improve the natural environment including forests, lakes, rivers and wildlife and to have compassion for living creatures.” The constitutional provisions are backed by a number of laws - acts, rules, and notifications like Factories Act 1948; (Prevention and Control of Pollution) Act 1974; Forest (Conservation) Act 1980; Air (Prevention and Control of Pollution) Act 1981; Water Biomedical waste (Management and Handling) Rules 1998; Municipal Solid Wastes (Management and Handling) Rules, 2000; Ozone Depleting Substances (Regulation and Control) Rules 2000; Noise Pollution (Regulation and Control) (Amendment) Rules 2002; Biological Diversity Act 2002. The Department of Environment was established in India in 1980 to ensure a healthy environment for the country. This later became the Ministry of Environment and Forests (MOEF) in 1985. The EPA (Environment Protection Act), 1986 came into force soon after the Bhopal Gas Tragedy and is considered an umbrella legislation as it fills many gaps in the existing laws.

The Ministry of Environment & Forest, Government of India (GOI), has brought a number of regulatory and non regulatory initiatives, in its efforts in harmonizing environmental protection with economic development. In 1991 GOI has made its first public announcement about the need for environmental disclosure in annual reports. In addition to the above requirement, companies are required to prepare director's report as per director’s report rules, 1988. Further, the Companies' Bill 1993 & 1997 had proposed the amendment of section 173 to disclose through its board of directors report the measures taken for protection of environment. There is also a mandatory requirement for Indian companies to report on conservation of energy, technology absorption, etc. in accordance with the provisions of Section 217 (1) (e) of the Indian Companies Act 1956.

In India, financial accounting & reporting guidelines are issued and governed by the Institute of Chartered Accountants of India (ICAI). Companies Act mandates the preparation of annual accounts of companies in accordance with the accounting standards issued by ICAI. Specific environmental accounting rules or environmental disclosure guidelines, for communication to different stakeholder groups, are not available for Indian companies. There is no mandatory requirement for quantitative disclosure of (financial) environmental information in annual reports neither under the Companies Act nor as per Indian Accounting Standards Further more there are 23 stock exchanges in India, governed by the Securities and Exchange Board of India (SEBI) Act 1992. Each of these stock exchanges has different listing requirements. However, there is no mandatory SEBI listing requirement for Indian companies, from these stock exchanges, to disclose environmental in-formation. Therefore, any environmental disclosure by Indian companies is purely voluntary.

Over the past decades companies have recognized the benefits of environmental reporting. As a result, there was dramatic increase in the number of companies reporting in numerous ways. It is important to understand as to how far standard setting improves credibility in reporting through major surveys. However, most studies are based on content analysis of annual reports.

Firstly, a survey by International accountancy firm KPMG (2005) shows that there is not just an increase in the number of corporate responsibility (CR) information in annual (financial) reports but also on the assurance. There are standards available for assurance on non -financial information like the International Standard for Assurance Engagements (ISAE) 3000, and Accountability’s AA1000 Assurance Standard. In 2005 survey number of companies issuing corporate responsibility reports is approximately 80% representing 21 nations in comparison to 2002 survey with only 50% companies in the reporting arena. This result supports the widespread understanding that multinational corporations publish more CR than other national companies. Prior research on internet based environmental disclosure concludes that multinational corporations of developed nations prefer digital reporting over print medium.

Secondly, GRI guidelines provide principles and detailed indicators for reporting on all aspects of CR performance. Sustainability Reporting Guidelines of the Global Reporting Initiative (GRI) developed through a multi-stakeholder process bring in dramatic increase in corporate reporting practices. There are 660 companies spread over 50 countries report on the basis of GRI guidelines. This widespread use of international guidelines by GRI assures comparability, which is one of the 11 major GRI Reporting Principles. Further, their study expects GRI guidelines to reap the following benefits such as: improved relationships with stakeholders; breaking down internal organizational insularity through information sharing; reduction of volatility and uncertainty in share prices; building brand image; and creation of competitive advantage.

Mitchell et al. (2006) examined the environmental disclosures of twenty Australian firms subject to a successful EPA prosecution between 1994 and 1998 using content analysis, finding the disclosures made by their sample firms to be predominantly positive in nature. Similarly, using content analysis, Cowan and Gadenne (2005) found a tendency by their sample Australian firms to disclose higher levels of positive environmental news. Finally, also using content analysis, Tilt (2001) found that even where a firm has a specific corporate environmental policy, they place a low priority on reporting environmental performance data to external parties. She concluded that Australian firms prefer to disclose their activities and specific programs, rather than their research and development, capital expenditure, policies or performance.

Bewley and Li (2000) appealed to voluntary disclosure theory to examine the environmental disclosures of Canadian manufacturing firms. They used the Wiseman index to measure the 1993 annual report disclosures of 188 firms and industry membership to proxy for pollution propensity. They found that firms with a higher pollution propensity and greater media coverage of their environmental performance are more likely to disclose general environmental information, a result also consistent with the socio-political theories. Similarly, Hughes et al. (2001) examined environmental disclosures made by U.S. manufacturing firms in 1992 and 1993 using a modified Wiseman index to measure disclosures in the president’s letter, MD&A, and notes sections of the annual report, and the CEP rankings to proxy for environmental performance. They found that firms rated as poor by the CEP generally make the most disclosures.

Al-Tuwaijri et al. (2004) employed simultaneous equations approach to investigate the relations among environmental disclosure, environmental performance and economic performance. They used proxy for environmental performance using the percentage of total waste generated recycled as identified using the TRI database and measure environmental disclosure using a content analysis in four categories, potential responsible parties’ designation, toxic waste, oil and chemical spills, and environmental fines and penalties, disclosures which are largely non-discretionary. Based on these proxies, Al-Tuwaijri et al. (2004) documented a positive association between environmental performance and environmental disclosure.

Daniel Mogaka Makori employed Department of Accounting and Finance School of Business Kenyatta university, Kenya, He was study Environmental Accounting and Firm Profitability: An Empirical Analysis of Selected Firms Listed in Bombay Stock Exchange, India in Environmental Accounting, Firm Profitability, Return on Capital Employed, Earnings per Share (EPS), Net Profit Margin and Dividend per Share.

Social performance information, social audit, social accounting, socio-economic accounting, social responsibility accounting and social and environmental reporting have been used interchangeably in the literature. Corporate environmental disclosure is a part of social reporting and the environmental disclosures are mainly non-financial in nature. The extent of literature on corporate disclosure focuses on the determinants of voluntary disclosure and on the effect of voluntary disclosures on return earnings relation. However, there is a lack of specific studies regarding Corporate Social and Environmental Disclosures (CSEDs) both in developed and developing countries.

Profitability as well as corporate financial performance was used by a number of researchers as an explanatory variable for differences in disclosure level. However, the relationship between corporate financial performance and corporate social and environmental disclosure is arguably one of the most controversial issues yet to be solved. The proponents argue that there are additional costs associated with the social and environmental disclosure and, the profitability of the reporting company is depressed.

Survey of empirical literature show that corporations are disclosing social and environment information in corporate annual reports and this has increased over years. It has been argued by the researchers that the level of Corporate Environmental Accounting and Disclosure is dependent on several corporate attributes and there are studies which empirically examined the extent of environmental disclosure and measured the relationship between environment disclosure and several corporate attributes. However, most of these studies concentrated on developed countries and very few studies focused on developing countries such as India. It has also been argued that corporate social and environmental disclosure may not apply universally to all countries which are in various stages of economic development and with corporations having differing levels of awareness and attitudes towards corporate environmental disclosure. It has also been observed that most of them were based on content analysis of annual reports. Content analysis is presently the most widely used technique for analysis of narratives in annual financial reports. Since this method is most used by authors, this study takes a little deviation from content analysis to examine the effect of the environmental accounting on profitability of selected Indian firms using multiple regression models.

6. Objective of the study:

The main objective of this study is to establish whether there is any significant relationship between environmental accounting and firm profitability in Reliance Industry Limited, Gujarat.

- To investigate whether there is any significant relationship between environmental accounting and Return on Capital Employed (ROCE).

- To establish whether there is significant relationship between environmental accounting and Net Profit Margin (NPM).

- To determine whether there is significant relationship between environmental accounting and Divided per share (DPS).

- To examine if there is significant relationship between environmental accounting and Earnings per Share (EPS).

- Ho1: There is no significant relationship between Environmental Accounting and Return on Capital Employed.

- Ho2: There is no significant relationship between Environmental Accounting and Net profit Margin.

- Ho3: There is no significant relationship between Environmental Accounting and Dividend per Share.

- Ho4: There is no significant relationship between Environmental Accounting and Earnings per Share.

In order to find out the relationship between different variables, the data were then analyzed using multiple regression analysis through the use of econometric model. The model is specified below:

Where: ENVC, ROCE, NPM, DPS and EPS represent Environmental Cost of Companies; Return on Capital Employed; Net Profit Margin; Dividend per Share; and Earnings per Share respectively.

The econometric form of the model is as follows:Where: a0+a1+a2+a3+a4 and ut represent intercept, Impact of Return on Capital Employed,

Impact of Net Profit Margin, Impact of Dividend per Share, Impact of Earnings per Share and Error terms respectively. The priori expectation is that Environmental Accounting has a positive relationship with the Return on Capital Employed (ROCE), Net Profit Margin (NPM) Dividend Per Share (DPS) and Earnings Per Share (EPS) in the period under study. Amount spent by each company as their environmental cost was used as proxy for environmental accounting while Return on Capital Employed (ROCE), Net Profit Margin (NPM), Dividend Per Share (DPS) and Earnings Per Share (EPS) were used as proxy for firm profitability.

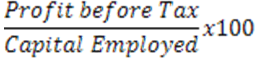

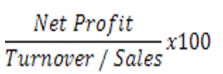

Data for this research study were secondary data generated from Annual Reports and Accounts of selected company quoted on the Reliance Industry Limited, Gujarat. The formulae for calculating the ratios are presented in table 1 below.

| Variables | Formula |

| Return on Capital Employed (ROCE) |  |

| Net Profit Margin (NPM) |  |

| Dividend Per Share (DPS) |  |

| Earning Per Share (EPS) |  |

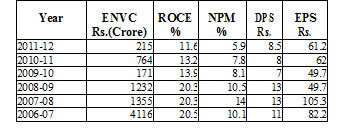

The results for different measures of environmental accounting and profitability of the firms including Return on Capital Employed, Net Profit Margin, Dividend Per Share and Earning Per Share are presented in the following section. First, the descriptive analysis is presented followed by multiple regression analysis to see the association between Net Operating Profitability and all independent variables. The data obtained from the various financial statements are presented in a tabular form as shown in table 2 below:

In analyzing the data presented in the above table, the ordinary least square regression method was used. The result of the data analysis is presented below.

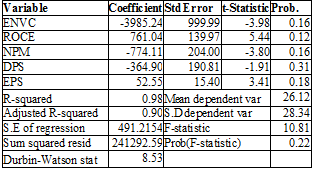

In table 3, From the result presented above, all the variables except Return on Capital Employed (ROCE) and Earnings Per Share (EPS) are in line with the apriori expectation. It can also be seen that Environmental Accounting has a positive relationship with the Net Profit Margin (NPM) and Dividend Per Share (DPS) and a negative relationship with Return on Capital Employed (ROCE) and Earnings Per Share (EPS) in the period under study. Using the Co-efficient of variation from the model presented above, it will be observe that autonomous Environmental Accounting which is represented by Environmental Cost (ENVC) is a negative 8839618 when all other variables are held constant.

Consequently, a unit change in Environmental Cost (ENVC) will lead to negative change of about 761.04 units in ROCE less the autonomous component provided all other variables arc held constant. Also, a unit change in ENVC provided all other variables are held constant will have a positive change of about -774.11 units in NPM less the autonomous component. Furthermore, a unit change in ENVC will lead to a positive change of about -364.90 units in DPS less the autonomous component. And a unit change in ENVC will lead to a negative change of 52.55 units in EPS.

Using the T- Ratio to test for their statistical significance, it is evident that only NPM and DPS variables are statistically significant. This is due to the fact that their observed T- values are positive and above the “rule of thumb of 2”. The other variables are statistically insignificant because their observed t-values are either negative or far less than the 'rule of thumb' of 2. From the R- squared of 0.98, the regression co-efficient indicates that about 83% of the changes in the dependent variable are explained by the changes in the independent variables. The F- value of 10.81 indicates that the parameter estimate cannot be dismissed at 5% level of significance. This is due to the fact that the calculated F- value is more than the critical K-value. The D.W statistic of 8.53 indicates the absence of auto - correlation since it is up to rule of Thumb of 2. In the course of this research, some hypotheses were formulated and they include:

Ho1: There is no significant relationship between Environmental Accounting and Return on Capital Employed.

Ho2: There is no significant relationship between Environmental Accounting and Net profit Margin.

Ho3: There is no significant relationship between Environmental Accounting and Dividend per Share.

Ho4: There is no significant relationship between Environmental Accounting and Earnings per Share.

To test for the above hypotheses, the researcher had to consider the test of significance, which is the F-statistic. The tool of F-statistic helps in determining the overall joint significant of the explanatory (independent) variables on the dependent or explained variable. At 5% level of significance, K critical or F tabulated is 0.001 when comparing this with the calculated value from the above table, which is 10.81. The decision rule is that, if the calculated value is greater than the tabulated, reject null hypothesis (Ho). Hence, the null hypotheses are rejected since f-cal (10.81) is greater than the f-tab (0.001). It indicates that the explanatory variables are jointly significant at explaining or causing much variation in the dependent variable (Environmental cost). The null hypothesis is therefore rejected, which mean that Environmental Accounting has significant relationship with the various variables used in measuring firm profitability. It is also necessary to note that this relationship with the variables of corporate performance is cither positive or negative.

9. Limitations of the StudyEmpirical research on corporate environmental disclosure is available largely for developed nations and very few is available for Asian countries. This research is probably one of the very few initial research works with respect to environmental accounting by Indian corporate.

Hence, the extent of prior research literature available on environmental accounting reporting by Indian companies is limited. The sample size considered for this research is too small to generalize and conclude for diverse sectors of Indian companies. There is scope for doing further theoretical and action research in this field.

Environmental costs cover all cost; incurred concerning environmental protection such as emissions treatment as well as wasted material, capital and labour which so called ‘non product output’ as a result of inefficiency production activities. Different firms may consider different elements into environmental costs but it is important that all significant and relevant costs are incorporated for sound decision making purpose. The general picture, which emerges from current reporting, is that since the disclosures of environmental information are voluntary, there is a diversity of reporting practice. Large companies tend to report more environment information in their annual reports than the medium-scale businesses; and the disclosure, tend to be more qualitative than quantitative despite the fact that there is a significant relationship between environmental accounting and Firm Profitability.

REFERENCES :

***************************************************

Prof. Chauhan Lalitkumar Rajnikant Kalola Rima A

Shri M. P. Shah Muni. College of Commerce

Jamnagar

Phd Scholar

Saurashtra University

Rajkot

Home | Archive | Advisory Committee | Contact us