Awareness Level of E-banking Among Customers

Abstract ::

The world is currently experiencing a foremost change i.e. "The Information Technology Revolution". The foundation stone of this revolution is the innovations and developments in Computing and Telecommunication Technologies. The effect of IT on service sector is large as compared to others. All over the world, the banking sector being a service provider has been observing a big change in its working environment, policies, organizational structure, service delivery channels and deployment of new products. Electronic Banking (e-banking) is a modern banking system. It is the accessibility of banking services in electronic form , which were traditionally available only at bank-counters and dispersed by the humans. E-banking is changing the ways of doing banking business with modern technologies and techniques. It is the replacement of traditional tools such as papers and pencils with electronic system. The e-banking is not limited to the cash withdrawal or funds transfer from one account to another. It includes all electronic platforms ranging from self-service terminals to internet and cell phones. This is a bouquet of all banking information or services that a customer desires from a financial organization. Current paper focuses on awareness of e-banking services among customers, various factors influencing the customers for using e-banking and problems identified by them.

Key Words:-E-banking, convenience, availability, money transfer, ATM

Introduction :

Indian Banking is the lifeline of nation and its people. Banking has developed vital sectors of the economy and usher in a new dawn of progress on the Indian horizon. The sector has translated the hopes and aspirations of millions of people into reality. But to do so, it had covered miles and miles of difficult terrain, suffer the indignities of foreign rule and the pangs of partition. Today Indian Banks can confidently compete with modern banks of the world. The first modern bank was founded in Italy in Genoa in 1406; its name was ‘Banco di San Giorgio’ (Bank of St. George).

Meaning of bank

A bank is like a reservoir into which flow the savings, the idle surplus money of households and from which loans are given an interest to businessman and others who need them for investment or productive uses.

Definition of bank

According to Indian Banking Regulation Act, 1949:

1) “A Banking Company (or a bank) is defined as “any company which transacts the business of banking in India.” [Section 5(1)]

2) “Banking” is defined as accepting, for the purpose of lending or investment, deposits of money from the public, repayable on demand or otherwise and withdraw able by cheque, draft, order or otherwise. [Section 5(2)]

Background of Indian banking system

In India, there prevailed a system of indigenous banking from very early times, though it was not similar to banking of modern times. There is evidence to show that money lending existed even during the Vedic period. With the advent of the English traders in the Seventeenth century and the establishment of trading centers by the East India Company, the position of indigenous bankers became precarious. Unable to use indigenous bankers for their trading and banking purposes, the East India Company, encouraged the establishment of agency houses-trading firms which undertook banking operations for the benefit of their constituents. Some of the important agency houses established during the period was Alexander & Co. & Fergusson & Co. These firms combined banking with other kinds of business and both were the predecessors of the early Joint Stock Banks in India. ‘The Bank of Hindustan’, a mere appendage of the former, was the earliest bank under European direction in India.

‘The Bank of Hindustan’ was the first bank in India, established in 1770. Since, 1770, the journey of Indian Banking System can be bifurcated into three distinct Phase.

Three distinct phases can be identified in the history of Indian banking. They are:

1. Pre-Nationalization period prior to 1969

2. Nationalization of banks and the period prior to banking sector reforms up to 1991

3. New phase of Indian banking with the advent of financial and banking sector reforms after 1991.

Overview of E –Banking System

The world is currently experiencing a foremost change i.e. “the Information Technology (IT) Revolution”. The foundation stone of this revolution is the innovations and developments in Computing and Telecommunication Technologies. What the steam engine did for our muscles, the modern computer is doing for our brain to manage information/data. The computer has been facilitating the Engineers, Doctors, Educationists, Researchers, Statistical Analysts and Bankers etc. to manage their valuable data/information and do complex calculations in easy, fast and reliable manner. The effect of IT on service sector is large as compared to others. All over the world, the banking sector being a service provider has been observing a big change in its working environment, polices, organizational structure, service delivery channels and deployment of new products.

The E-Banking is not limited to the cash withdrawal or funds transfer from one account to another. It includes all electronic platforms ranging from self-service terminals to Internet and cell phones. This is a bouquet of all banking information or services that a customer desires from a financial organization (Singh, 2002). The E-Banking means different facilities to the various users. Here users may be classified as bank customers and employees. Further there is categorization of customers into Individual Customers and Corporate Customers. Similarly the bank employees are divided into various categories of users as per their job nature and positions in all the three levels in the management such as Chairman, CEOs (Chief Executive Officers), Managing Directors, Regional/ Zonal/ Branch Managers, System Administrators, DBA (Database Administrator), Programmers and Data Entry Operators/Clerks etc.

Electronic Banking (E-Banking/e-Banking) is a modern banking system. It is the accessibility of banking services in electronic form, which were traditionally available only at bank-counters and dispersed by the humans. E-Banking is changing the ways of doing banking business with modern technologies and techniques. It is the replacement of traditional tools such as papers and pencils with the electronic systems. The introduction of Internet in the business has further enhanced the capacity and capability of overall banking system in terms of productivity, profitability, efficiency, quality of service and cost effective delivery of numerous products/services. Information regarding money, its storage in the computers in digital form and its movement anywhere in the world without considering physical boundaries is described as digital money and this whole process as Electronic Banking.

Delivery Channels in Electronic Banking System

The Delivery Channels are the means/modes through which the customers can transact their financial activities with the bank or online trading with third party. The convergence of Communication and Information Technologies in business sector especially in banking sector have innovated many electronic delivery channels. These electronic devices are being heavily used in banking as service delivery channels as per the convenience of customers in terms of time and place. In addition to above, the IT-Savvy Banks have been deploying electronic cards viz. Credit Cards, Debit Cards and Smart Cards etc. to provide more convenience to the customers in terms of availability of cash and online purchasing.

The technological developments have resulted in deployment of numerous delivery channels and electronic services such as:

1) Automated Teller Machines (ATMs) onsite or offsite,

2) Tele-Banking,

3) Internet Banking,

4) Mobile Banking,

5) Electronic Funds Transfer;

6) Magnetic Ink Character Recognition (MICR) based Cheque Clearing Systems,

7) Real Time Gross Settlement System,

8) Centralized Funds Management System (CFMS), and

9) Electronic Clearing Service (ECS).

Building Block of E-Banking

The foundation pillar of E-Banking is the automation of banking operations, processes, data and services into digital form. The computerization or automation of bank branch means digitization of processes/ information in addition to inter-connectivity with other players of banking system to exchange information by sharing infrastructure. The computerization of branch is the main requisite condition to move towards online banking or E-Banking but automation in isolated form does not play active role. The main objective of E-Banking is to provide right information to the right user (customer or bank) at the right time and at the right place. The e-Banking is the consolidation and accessibility of all branches’ database at a central location by using distributed database-computing technology. In addition to this, it uses data mining and data warehousing technologies on consolidated customers’ database to facilitate the strategic planners to identify potential customers, markets and possibilities of emerging opportunities and risks.

The whole system of E-Banking is dependent on the following pillars:

-

Computing Technologies

-

Inter-connectivity

-

Content

-

Users

-

Trust and Security

-

Legal framework

E-Banking Characteristics

As the businesses are becoming increasingly digitised, the business models of financial institutions are also changing very fast. Banking is a business activity and E-Banking is its digital form, so E-Banking model is different than the traditional banking system.

The following are the characteristics of modern banking system i.e. E-Banking (Deutsche Bundesbank, 2000):

-

The transaction in electronic banking is no longer confined within the national borders due to their virtual nature i.e. electronic commerce based transactions. This intends that the banks need to cooperate even more closely with foreign bank’s authorities than in the past.

-

The secure and efficient deployment of ICT has become the crucial strategic factor for the success of electronic banking. Every stage of E-Banking since its implementation, operations, development, production of products and services, and their availability in market are entirely dependent on IT. More importantly, the banks’ dependency on innovative channels and particularly on internet increases the strategic and operational risks for the banks.

-

The innovative cycles for new products on the Internet are becoming shorter and shorter due to rapid pace of technological changes. In some cases, the technology behind some products is already obsolete well before those products are ready for marketing.

-

Technology and the increased market transparency reduce the information opaqueness between the bank and its customers. Thus, the existence of Internet causes the shift of banks’ power towards the customers. The customers are being provided a very high quality of service, short answering times and user-friendly banking services. Besides, E-Banking facilitates the customers to make easy access to several banks at a time, faster transactions which are not tied to specific locations and specific opening hours.

-

Several factors have conspired to include this effect. The greater ease with which prices and products can be compared has in turn enhanced the market transparency. The market entry barriers for the new competitors have been lowered. The internet and online customers display little brand loyalty and E-Banking customers are focusing even more on costs and profit margins.

Experience of India on E-Banking

India is still in the early stages of E-banking growth and development. Competition and changes in technology and lifestyle in the last five years have changed the face of banking. The issue here is – 'Where does India stand in the scheme of E-banking.' E-banking is likely to bring a host of opportunities as well as unprecedented risks to the fundamental nature of banking in India.

The impact of E-Banking in India is not yet apparent. Many global research companies believe that E-banking adoption in India in the near future would be slow as compared to other major Asian countries. Indian E-banking is still nascent, although it is fast becoming a strategic necessity for most commercial banks, as competition increases from private banks and non banking financial institutions.

The Reserve Bank of India had also set up a "Working Group on E-banking to examine different aspects of E-banking. The group focused on three major areas of E-banking i.e. (1) Technology and Security issues (2) Legal issues and (3) Regulatory and Supervisory issues. RBI has accepted the guidelines of the group and they provide a good insight into the security requirements of E-banking. The importance of the impact of technology and information security cannot be doubted. Technological developments have been one of the key drivers of the global economy and represent an instrument that if exploited well can boost the efficiency and competitiveness of the banking sector. However, the rapid growth of the Internet has introduced a completely new level of security related problems. The problem here is that since the Internet is not a regulated technology and it is readily accessible to millions of people, there will always be people who want to use it to make illicit gains. The security issue can be addressed at three levels. The first is the security of customer information as it is sent from the customer's PC to the Web server. The second is the security of the environment in which the Internet banking server and customer information database reside. Third, security measures must be in place to prevent unauthorized users from attempting to long into the online banking section of the website.

Regarding the regulatory and supervisory issues, only such banks which are licensed and supervised and have a physical presence in India will be permitted to offer E-banking products to residents of India. With institutions becoming more and more global and complex, the nature of risks in the international financial system has changed. The Regulators themselves who will now be paying much more attention to the qualitative aspects of risk management have recognized this.

Though the Indian Government has announced cyber laws, most corporate are not clear about them, and feel they are insufficient for the growth of E-commerce. Lack of consumer protection laws is another issue that needs to be tackled, if people have to feel more comfortable about transacting online.

Thus efficiency, growth and the need to satisfy a growing tech survey consumer base are three clear rationales for implementing E-banking in India. The four forces-customers, technology, convergence and globalization have the most important effect on the Indian financial sector and these changes are forcing banks to redefine their business models and integrate technology into all aspects of operation.

2. REVIEW OF LITERATURE

E-banking has been conceptualized and defined differently by the different scholars. Some of the definitions of the E-Banking in various aspects of banking and their nature of service are given below:

-

The E-Banking is flexible and user-friendly platform that provides integrated form of services to the customers irrespective of time and place in cost effective and efficient manner. This system is more accountable and responsible than the traditional system.

-

The E-Banking is to give more freedom to customers as there is no restriction on when and where availability of the service. The services are available as per the needs and requirements of the customers and banks themselves.

-

The E-Banking is a modern decision making approach with an ability to adopt ever-changing environment.

Rothwell and Gardiner (1984) observed that there are two fundamental sets of factors affecting user needs, namely price factors and non-price factors.

On the other hand, Guadagni and Little (1983), Gupta (1988), Mazursky et al., (1987) identified price as a major factor in brand switching. If consumers are to use new technologies, the technologies must be reasonably priced relative to alternatives. Otherwise, the acceptance of the new technology may not be viable from the standpoint of the consumer. In view of the Malaysian Government encouragement to move towards the digital era essential costs (access and connection) have been kept at a minimum.

White and Nteli (2004) conducted a study that focused on why the increase in Internet users in the UK had not been paralleled by the increase in Internet usage for banking purposes. Their results showed that customers still have concerns with the security and the safety aspects of the Internet.

Chung, et. al. (2002) in a survey on Internet banking in New Zealand confirmed the fact that security and complication of Internet banking are some of the factors limiting the full acceptance of Internet banking.

A study conducted on adoption of technology attempted to compare the adoption of retailing technology by elderly and non-elderly customers (Zeitaml and Gilly, 1987). They found the main reason for not using the ATMs to be their preference for personal transahuman tellers.

Marshall and Heslop (1988) found that consumers’ motives for use of technology are useful for predicting subsequent usage. Demographic factors such as higher education levels and employment status are positively related to usage of ATMs, whereas age of the users was negatively related to adoption of ATMs.

Al-Ashban and Burney (2001) In their study among the Saudi Arabian consumers regarding the usage of tele-banking services, found that the Saudi consumers’ age, income levels and education are prime factors determining their adoption and usage. In addition to this they found that customers tend to increase their usage of tele-banking services depending on their past experience. They concluded that tele-banking has resulted in substantial cost savings for the banks and has given rise to increasing convenience for the increasingly discerning consumers.

Mattila (2001)They found out in Finland that typical users of Internet banking were well-educated male professionals between the ages of 35 to 40. Elderly people especially females over 50 were reluctant to use the IB service. Elderly people associated a bank transaction with human transaction. Experience with computers was a major driver for IB use. Surprisingly security was not a major concern for non-use.

Karjaluoto et al. (2002) The findings of their research conducted amongst Finnish bank customers showed that ‘prior experience’ with computer and technology along with ‘attitudes’ towards computer, influence both attitude and behavior towards online banking. Since it is found that prior computer experience had a strong influence on Internet banking usage it is advised by them that banks should give training to its customers not only in the usage of Internet but also in the usage of computers.

Mookerji (1998) explored that Internet banking is fast becoming popular in India. Nevertheless, it is still in its evolutionary stage. They expect that a large sophisticated and highly competitive Internet banking market will develop in future.

Joseph et al. (1999) examined the influence of Internet on the delivery of banking services. They found six primary dimensions of e-banking service quality such as convenience and accuracy, feedback and complaint management, efficiency, queue management, accessibility and customization.

Mishra (2005) in his paper explained the advantages and the security concerns about Internet banking. According to him, improved customer access, offering of more services, increased customer loyalty, attracting new customers are the primary drivers of Internet banking. But in a survey conducted by the online banking association, member institutions rated security as the most important concern of online banking.

3. Research Methodology

Scope of the Study

Scope of the study is limited to 50 participants of ASC,HPU, Shimla. Study focuses on various aspects viz. Awareness of E-banking, Preference of transaction, and Identification of various problems faced by academicians while using E-banking.

Objectives of the Study

The research aims at enriching the knowledge and understanding of factors effecting the adoption of e- banking in India.

Following are the objectives of the study.

1. To Study awareness of e-banking services among ASC participants, HPU, Shimla.

2. To examine various factors which influence the customers for using e-banking services.

3. To analyse the problems identified by customers while using e-banking services.

Hypothesis of the Study

H0: There is no significant relationship between gender and factors influencing use of E-banking.

Ho: There is no significant relationship between gender and Problems faced while using E-banking services.

H0: There is no significant relationship between gender and preference for transactions of E-banking services

Ho: There is no significant relationship between gender and satisfaction level.

Data Collection

The study is based on both primary and secondary sources of data. Primary data is collected through field survey by getting questionnaire filled from respondents.

Secondary data in this research work is collected through books, journals, magazines, newspapers and Internet website etc.

Sample Size

The present study is based on data collected through questionnaire distributed among 50 participants of academic staff college coming from different states.

Analysis of Data

The data collected was processed using the Statistical Package of Social Science (SPSS) 18.0 computer software. In this project Frequency Distribution, Descriptive Statistics Analysis:, Chi-square Test, Population Proportion Test, Difference between two Population Proportion Test are applied to analyse the result.

4. Analysis and Interpretation

Respondents were asked various questions regarding awareness of E-banking services, various factors which influence them for using E-banking services and various problems faced by them while using E- banking services.

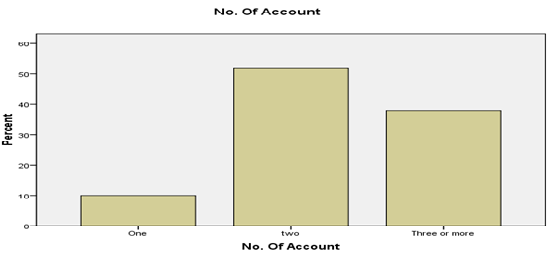

No. of Bank Accounts

Table 1: No. of Bank Accounts

|

|

|

Frquency |

Percent |

Valid Percent |

Cumulative Percent |

| Valid |

One |

5 |

10.0 |

10.0 |

10.0 |

| Two |

26 |

52.0 |

52.0 |

62.0 |

| Three or more |

19 |

38.0 |

38.0 |

100.0 |

| Total |

50 |

100.0 |

100.0 |

|

Figures given in table-1 show No. of accounts the respondents are having, It was found that 10% of the respondents have only one account, where as 52% of the respondents have two accounts and 38% of the respondents have three or more than three accounts.

It is clear from the above Bar diagram that majority of the respondents prefer to have only two accounts.

Types of Bank

Table 2: Types of Bank

| Types of Bank |

|

Frequency |

Percentage |

| PSU Bank |

Not Have |

4 |

8.0 |

| |

Have |

46 |

92.0 |

| |

Total |

50 |

100.0 |

| Private Bank |

Not Have |

34 |

68.0 |

| |

Have |

16 |

32.0 |

| |

Total |

50 |

100.0 |

| Foreign Bank |

Not Have |

47 |

94.0 |

| |

Have |

3 |

6.0 |

| |

Total |

50 |

100.0 |

| Co-operative Bank |

Not Have |

44 |

88.0 |

| |

Have |

6 |

12.0 |

| |

Total |

50 |

100.0 |

Figures given in table-2 reveal that 92% of the respondents prefer to have accounts with PSU bank, where as 68% of the respondents prefer private bank over others. Only 6% of the respondents prefer to open account with foreign bank.Whereas 12% of the respondents prefer co-operative bank.

Awareness of services provided by bank

Following table indicates level of awareness among respondents regarding E-banking services available. As far as facility of ATM, debit card, credit card and internet banking is concerned more than 50% of the respondents are aware about it where as only 38% of the respondents are aware about phone banking.

Table 3: Awareness of services provided by bank

| Service |

Not Aware |

Aware |

| ATM |

7 (14%) |

43

(86%) |

| Debit Card |

12

(24%) |

38 (76%) |

| Internet Banking |

16

(32%) |

34 (68%) |

| Credit Card |

22

(44%) |

28

(56%) |

| Phone Banking |

31

(62%) |

19

(38%) |

| Mobile Banking |

19

(38%) |

31 (62%) |

Present work supplements a research done in Hongkong by Wan as they as they found that ATM was the most frequently adopted channel, followed by internet banking and telephone banking was the least frequently adopted.

Factors influencing use of E-banking services

H0: There is no significant relationship between gender and factors influencing use of E-banking.

Table 4: Factors influencing use of E-banking services

| Factors |

Gender |

Strongly |

More than average |

Average |

Less than Average |

Not at all |

Pearson Chi-Square |

P-value |

| 24*7 OR All time available |

Male |

42.0% |

12.0% |

10.0% |

.0% |

2.0% |

6.814a |

.078 |

| Female |

20.0% |

.0% |

14.0% |

.0% |

.0% |

| Ease of use |

Male |

38.0% |

20.0% |

8.0% |

.0% |

.0% |

3.795a |

.150 |

| Female |

28.0% |

6.0% |

.0% |

.0% |

.0% |

| Convenience |

Male |

38.0% |

16.0% |

12.0% |

.0% |

.0% |

2.568a |

.277 |

| Female |

24.0% |

2.0% |

8.0% |

.0% |

.0% |

| Secured transaction |

Male |

8.0% |

26.0% |

14.0% |

.0% |

18.0% |

6.892a |

.075 |

| Female |

4.0% |

24.0% |

6.0% |

.0% |

.0% |

| Direct access |

Male |

32.0% |

22.0% |

12.0% |

.0% |

.0% |

1.813a |

.404 |

| Female |

22.0% |

10.0% |

2.0% |

.0% |

.0% |

| Friends/ Relatives |

Male |

12.0% |

14.0% |

34.0% |

4.0% |

2.0% |

5.564a |

.234 |

| Female |

6.0% |

16.0% |

8.0% |

4.0% |

.0% |

| Status symbol |

Male |

4.0% |

36.0% |

12.0% |

2.0% |

12.0% |

5.577a |

.233 |

| Female |

.0% |

14.0% |

16.0% |

.0% |

4.0% |

Responses were sought from customers on 5 point scale on various factors which influence them for using E-banking. It was found that “All time availability”, “Convenience” and “Ease of use” are the major factors which influence them to use E-banking. Very less percentage of respondents use E-banking as a status symbol.

It was hypothesised that there is no significant relationship between gender and factors influencing use of E-banking. P-values shown in the table-4 prove null hypothesis to be true. Some of the respondents are of the view that E-banking is more accountable and more responsible than the traditional system of the banking.

Problems faced while using E-banking services

Ho: There is no significant relationship between gender and Problems faced while using E-banking services.

Table 5 : Problems faced while using E-banking services

| Problems |

Gender |

Strongly |

More than average |

Average |

Less than Average |

Not at all |

Pearson Chi-Square |

P-value |

| Time Consuming |

Male |

6.0% |

14.0% |

10.0% |

18.0% |

18.0% |

7.035a |

.134 |

| Female |

6.0% |

4.0% |

14.0% |

8.0% |

2.0% |

| Insecure |

Male |

20.0% |

24.0% |

14.0% |

4.0% |

4.0% |

3.600a |

.463 |

| Female |

4.0% |

12.0% |

8.0% |

4.0% |

6.0% |

| ATM out of Order |

Male |

14.0% |

26.0% |

10.0% |

16.0% |

.0% |

11.107a |

.025 |

| Female |

16.0% |

12.0% |

.0% |

2.0% |

4.0% |

| Amount Debited but not withdrawn |

Male |

16.0% |

8.0% |

12.0% |

14.0% |

16.0% |

9.782a |

.044 |

| Female |

10.0% |

14.0% |

2.0% |

8.0% |

.0% |

| Problem of cheque in mobile no |

Male |

4.0% |

10.0% |

26.0% |

16.0% |

10.0% |

15.222a |

.004 |

| Female |

6.0% |

20.0% |

6.0% |

.0% |

2.0% |

| Password forgotten |

Male |

10.0% |

12.0% |

10.0% |

18.0% |

16.0% |

20.291a |

.000 |

| Female |

.0% |

20.0% |

14.0% |

.0% |

.0% |

| Card misplaced |

Male |

6.0% |

18.0% |

18.0% |

14.0% |

10.0% |

14.581a |

.006 |

| Female |

.0% |

28.0% |

4.0% |

.0% |

2.0% |

| Misuse of card |

Male |

2.0% |

16.0% |

20.0% |

18.0% |

10.0% |

9.124a |

.058 |

| Female |

2.0% |

22.0% |

6.0% |

2.0% |

2.0% |

The above table-5 indicates that 30% of the respondents have identified “ATM out of order” as a major problem while using ATM and 20% of the respondents have given “Amount debited but not withdrawn” as a major problem where as 24% of the respondents responded that “ Insecurity” is a major problem. One of the research studies in the U.K. also focused on the security issue and found that customer still have concern with the security and safety aspects of the internet. One of the surveys in New Zealand confirms the fact that security and complication of internet banking are some of the factors limiting the full acceptance of internet banking.

P-values in case of “Time consuming”, “Insecurity” and “Misuse of card” are more than 0.05 which means null hypothesis is accepted. It indicates that there is no significant relationship between gender and above mentioned problems while using E-banking. In case of problems like “ATM out of order”, “Problem of check in mobile number”, “Password forgotten”, and “Card misplaced” significant relationship is found between gender and problems while using E-banking as indicated by P-values which are less than 0.05. Therefore null hypothesis is rejected.

Preference of transactions in E-banking services

H0: There is no significant relationship between gender and preference for transactions of E-banking services

Table 6: Preference of transactions in E-banking services

| Transactions |

Gender |

Strongly |

More than average |

Average |

Less than Average |

Not at all |

Pearson Chi-Square |

P-value |

| Money Transfer |

Male |

6.0% |

14.0% |

10.0% |

24.0% |

12.0% |

6.541a |

.162 |

| Female |

10.0% |

2.0% |

6.0% |

6.0% |

10.0% |

| Checking of your current balance |

Male |

8.0% |

6.0% |

22.0% |

30.0% |

0% |

4.691a |

.196 |

| Female |

.0% |

.0% |

18.0% |

16.0% |

0% |

| Create fixed deposit online |

Male |

22.0% |

16.0% |

18.0% |

10.0% |

.0% |

14.848a |

.005 |

| Female |

14.0% |

6.0% |

.0% |

4.0% |

10.0% |

| Request a Demand Draft |

Male |

22.0% |

14.0% |

10.0% |

18.0% |

2.0% |

11.575a |

.021 |

| Female |

14.0% |

.0% |

6.0% |

4.0% |

10.0% |

| Pay Bills |

Male |

10.0% |

14.0% |

10.0% |

20.0% |

12.0% |

4.863a |

.302 |

| Female |

.0% |

8.0% |

2.0% |

12.0% |

12.0% |

| Order a cheque book |

Male |

18.0% |

12.0% |

4.0% |

20.0% |

12.0% |

8.400a |

.078 |

| Female |

14.0% |

4.0% |

2.0% |

.0% |

14.0% |

| Request a Stop payment on a cheque |

Male |

16.0% |

22.0% |

16.0% |

4.0% |

8.0% |

14.880a |

.005 |

| Female |

8.0% |

6.0% |

.0% |

.0% |

20.0% |

As shown in the above table 58% of the respondents prefer to create “Fixed Deposit online”, 52 % of the respondents prefer to “Request stop payment on a cheque”, 50% of the respondents prefer “Online facility of demand draft” and 48% of the respondents prefer to “order a cheque book” through E-banking. “Money transfer”, “checking of current balance” and “Paying bills” are the least preferred transaction through E-banking.

P-values (see table-6) indicate that there is no significant relationship between gender and transaction preferred in case of “Money transfer”, “Checking of current balance”, “Pay bills” and “Order a cheque book” therefore null hypothesis is accepted in these cases.

Education provided by Bank regarding E-banking Services

Responses were sought from customer with regard to education provided by their bank regarding E-banking services.

Table 7: Education provided by Bank regarding E-banking Services

| Education provided by bank |

Frequency |

Percent |

| Yes |

25 |

50.0 |

| No |

25 |

50.0 |

| Total |

50 |

100.0 |

Percentages given in table-7 reveal that 50% of the respondents said that their banks provide them education regarding E-banking services where as 50% of the respondents said that their banks do not provide them E-banking education. Therefore it can be said that lack of awareness may be one of the reasons that customers prefer only limited services of E-banking.

Level of satisfaction

Responses were also sought from respondents with regard to their satisfaction level with respect to E-banking services enjoyed by them.

Table 8: Level of satisfaction

| Responses |

Frequency |

Percent |

| Highly Satisfied |

11 |

22.0 |

| Satisfied |

36 |

72.0 |

| Neutral |

3 |

6.0 |

| Total |

50 |

100.0 |

Mean: 1.84

Std. Deviation: .510

Skewness -.272

Kurtosis: .549

Figures given in table-8 highlight that 94% of the respondents are satisfied with respect to E-banking services provided by their bank. This is also supported by negative value of Skewness (-.272) which shows that opinions of respondents are more towards the higher side i.e majority of the respondents are satisfied with E-banking services provided by their banks.

Ho: There is no significant relationship between gender and satisfaction level.

Table 9: Satisfaction of E-banking Cross tabulation

| Gender |

|

Highly Satisfied |

Satisfied |

Neutral |

Total |

| Male |

% of Total |

10.0% |

52.0% |

4.0% |

66.0% |

| Female |

% of Total |

12.0% |

20.0% |

2.0% |

34.0% |

| Total |

% of Total |

22.0% |

72.0% |

6.0% |

100.0% |

Chi- square value 2.691

P-value .260

Further to test whether there is significant relationship between gender and satisfaction level towards E- banking Chi- Square was applied. P-value (0.260) shown in table-9 indicate that there is no significant relationship between gender and satisfaction level with respect to E-banking services. Percentage result show that 62% of the male and 32% of the female are satisfied with E-banking.

5. Conclusion

It is concluded that E-banking adoption is becoming popular among people. It is becoming strategic necessity even for most commercial banks. E-banking has brought host of opportunities as well as unprecedented risk to the fundamental nature of banking in India. People are using E-banking mainly because of its convenience and 24 hours availability and more over it is easy to use. ATM and Debit Card are most frequently adopted channel followed by internet banking. Though people prefer to go for E-banking but they are even scared of doing transaction through E-banking because of security reason. In a survey conducted by the online banking association, member institution also rated security as the most important concern of online banking.

Some of the respondents suggested that banks should increase withdrawal limit in ATM. Facility of TDS certificates on internet banking should also be provided bio-metric technique for security is also recommended by many of the respondents. Banks should also provide information about latest schemes of the banks through E-banking services.

REFERENCES :

-

Al-Ashban, A. A. and Burney, M. A. (2001) “Customer adoption of telebanking technology: the case of Saudi Arabia”, International Journal of Bank Marketing, Vol 19, No.5, pp 191-200.

-

Chung, W. and Paynter, J. (2002). An Evaluation of Internet Banking in New Zealand. In Proceedings of 35th Hawaii Conference in System Sciences (HICSS 2002), IEEE Society Press.

-

Hasan I (2002), “Do Internet Activities Add Value? The Italian Bank Experience”, Working Paper, Federal Reserve Bank of Atlanta, New York University.

-

Joseph, M., McClure, C. and Joseph, B. (1999), “Service quality in the banking sector: the impact of technology on service delivery”. International Journal of Bank Marketing, Vol.17, No 4,pp 182-191.

-

Karjaluoto, H., Mattila, M. and Pento, T. (2002),”Factors underlying attitude formation towards online banking in Finland”, International Journal of Bank Marketing, Vol. 20, No.6, pp 261-272.

-

Marshall, J. J. and Heslop, L. A. (1988), “Technology Acceptance in Canadian retail banking: a study of consumer motivations and the use of ATMs”, International Journal of Bank Marketing, Vol. 6, No.4.pp 31-41.

-

Mattila, M., Karjaluoto, H., and Pento, T. (2001), “Internet Banking Adoption Factors in Finland”, Journal of Internet Banking and Commerce, Vol. 6, No.1, e-journal, accessed through www.arraydev.com

-

Mishra A K (2005), “Internet Banking in India Part-I”, http://www.banknetindia.com/banking/ibkg.html (15 Sept. 2010)

-

White H and Nteli, F. (2004) Internet banking in the UK: Why are there not more customers? Journal of Financial Services Marketing

-

Wan, W. W. N., Luk, C. L. and Chow, C. W. C. (2005) “ Customers’ Adoption of banking Channels in Hong Kong” International Journal of Bank Marketing, Vol. 23, No. 3, pp 255-272.

Web site

-

http://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/21595.

-

http://www.arraydev.com/commerce/jibc/0001-03.htm

-

http://www.encyclopedia4u.com/b/bank.html

-

http://www.expresscomputeronline.com/20021202/banks1.shtml

-

http://www.buba.de/download/volkswirtschaft/mba/2000/200012mba_art03_ebanking.pdf

-

www.Banknetindia.com

-

www.rbi.com

***************************************************

DR. JIGNESH P. VAGHELA

R.V.Patel College of Commerce, Amroli, Surat

DR. KHUSHDIP KAUR

Khalsa College for Women, Punjab

MUKESH R. GOYANI

R.V.Patel College of Commerce, Amroli, Surat

|