CONVERGENCE OF INDIAN ACCOUNTING STANDARDS TOWARDS IFRS

Abstract ::

The word social responsibility means to help the society in every manner as well as social accounting is attracting the attention of many industrialists today as a result of industrial growth & economic prosperity of many nations. If an organization has to function effectively and survive, it has to be accountable to the public at a large. Many Indian companies have given “value added statement” and sustainability reports in their annual reports in place of social reporting.

Social accounting is a method by which a firm seeks to place a value on the impact on society of its operations. The effect on society of the packaging it produced share holders, mandatory social disclosure requirement and management’s motivation to improve the firm image more & more corporations of developed countries.

Key words: Social Accounting, Human resource contribution, Foreign Exchange, Multi Perspective

Introduction ::

The convergence of accounting standards towards IFRS is gaining momentum across the globe and accounting bodies such as the International Accounting Standards Board (IASB) and US Financial Accounting Standards Board (FASB) have already initiated the groundwork on converging International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP). Many countries have recognized the need for convergence of accounting standards and are moving towards its implementation. Convergence to IFRS will greatly enhance an Indian entities’ ability to raise and attract foreign capital. Introduction of IFRS represents a fundamental change in financial reporting. Various systematic steps like generating the necessary awareness, educating stakeholders and managing the required changes will take considerable management commitment and time to achieve a successful transition. A low cost, a common accounting language, such as IFRS, will help Indian companies benchmark to their performance with global counterparts. Companies need to conduct a diagnostic study before proceeding for a full IFRS conversion. The Timeline for convergence of India’s GAAP with IFRS is April 1, 2011, companies started adopting the standards from FY10 itself so that comparative figures would be available for disclosure in the annual report. A successful transition requires a well-thought-of plan and hopefully well in advance. Many large listed companies have already moved on to the new standards and those that are in transition must be actively incorporating the change, especially in the beginning of the new financial year.

Need for IFRS ::

Level of Confidence: The key benefit will be a common accounting system that is perceived as stable, transparent, and fair to investors across the world, whether local or foreign.

Risk Evaluation: IFRS will eliminate barriers to cross-border listings and will be beneficial for investors.

Merger & Takeover Activity: Cross-border mergers and acquisitions will get a boost by making it easier for the parties involved in as far as rewarding the financial statement is concerned.

Investments: Foreign investors will be attracted to economies where IFRS- compliant financial statements are the norm.

IFRS in India ::

International Financial Reporting Standards (IFRS) convergence, in recent years, has gained momentum all over the world. As the capital markets become increasingly global in nature, investors feel the need for a common set of accounting standards.

India being a key global player, migration to IFRS will enable Indian entities to have access to international markets without having to go through the cumbersome conversion and filing process. It will lower the cost of raising funds, reduce accountants' fees and enable faster access to all major capital markets. Furthermore, it will facilitate companies to set targets and milestones based on a global business environment, rather than an inward perspective.

Furthermore, convergence to IFRS, by various group entities, will enable management to bring all components of the group into a single financial reporting platform. This will eliminate the need for multiple reports and significant adjustment for preparing consolidated financial statements or filing financial statements in different stock exchanges.

IFRS: Growing a Roadmap to Convergence ::

Convergence of accounting standards across the globe is gaining increasing momentum. Thus, while the International Accounting Standards Board (IASB) and the U.S. Financial Accounting Standards Board (FASB) continue to work closely on converging International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Standards in the United States (U.S. GAAP), the Institute of Chartered Accountants of India (ICAI) has released a 'Concept Paper on Convergence with IFRS in India', which details the strategy and roadmap for convergence of Generally Accepted Accounting Standards in India (Indian GAAP) with IFRS effective April 1, 2011. Most standard-setting bodies have acknowledged that the ultimate goal of convergence is to have a single globally accepted financial reporting system. A combination of proposed convergence of national standards with IFRS and the direct use of IFRS in more than 100 countries means that the accounting languages of the world may ultimately converge to IFRS.

The convergence momentum has been accelerated by the decision of the U.S. Securities and Exchange Commission (SEC) to permit foreign companies listed in the U.S. to present financial statements in accordance with IFRS and a Concept Release by the SEC to permit U.S. domestic companies a choice to adopt IFRS.

These developments have triggered an emerging debate amongst corporate prepares, professionals, standard-setters and regulators in India, on the impact of these developments on corporate India. For example, the following questions have been raised and are being debated :

Worldwide Momentum ::

The international standard-setting process began several decades ago as an effort by industrialized nations to create standards that could be used by developing and smaller nations unable to establish their own accounting standards. But as the business world became more global, regulators, investors, large companies and auditing firms began to realize the importance of having common standards in all areas of the financial reporting chain. In a survey conducted in late 2007 by the International Federation of Accountants (IFAC), a large majority of accounting leaders from around the world agreed that a single set of international standards is important for economic growth. Of the 143 leaders from 91 countries who responded, 90% reported that a single set of international financial reporting standards was “very important” or “important” for economic growth in their countries. Currently, more than 120 nations and reporting jurisdictions permit or require IFRS for domestic listed companies. The European Union (EU) requires companies incorporated in its member states whose securities are listed on an EU-regulated stock exchange to prepare their consolidated financial statements in accordance with IFRS.1 Australia, New Zealand and Israel have essentially adopted IFRS as their national standards.2 Brazil started using IFRS in 2010. Canada adopted IFRS, in full, on Jan. 1, 2011. Mexico will require adoption of IFRS for all listed entities starting in 2012. Japan is working to achieve convergence of IFRS and began permitting certain qualifying domestic companies to apply IFRS for fiscal years beginning April 1, 2010. A decision regarding the mandatory use of IFRS in Japan is to be made around 2012. Hong Kong has adopted national standards that are equivalent to IFRS and China is adopting its accounting standards with IFRS. Other countries have plans to adopt IFRS to their national standards. In addition to the support received from certain U.S.-based entities, financial and economic leaders from various organizations have announced their support for global accounting standards. Leaders of the Group of 20 (G20) called for global accounting standards and urged the U.S. Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) to complete their convergence projects in 2011. A summary of the IASB and FASB efforts regarding convergence is subsequently described

INDIA’S ROADMAP TO CONVERGENCE ::

In line with the global trend, the ICAI has recently proposed a plan for convergence with IFRS for certain defined entities (listed entities, banks and insurance entities and certain other large-sized entities) with effect from accounting periods commencing on or after April 1, 2011. Large-sized entities are defined as entities with turnover in excess of Rs.1 billion or borrowings in excess of Rs.250 million. For other small and medium sized entities (SME), the ICAI has proposed the application of the proposed International Financial Reporting Standard for SME' (with or without modifications). The proposed standard represents a simplified set of standards for SME' with disclosure requirements reduced, methods for recognition and measurement simplified and topics not relevant to SME eliminated. The convergence plan and strategy proposed by the ICAI is detailed in its Concept Paper on Convergence with IFRS in India.

Given that accounting standard-setting in India is subject to direct or indirect oversight by several regulators such as the National Advisory Committee on Accounting Standards (NACAS) established by the Ministry of Corporate Affairs, Government of India, the Reserve Bank of India (RBI), the Insurance Regulatory and Development Authority (IRDA) and the Securities and Exchange Board of India (SEBI), the ICAI would need to work closely with these regulators on the roadmap to convergence. Adoption of IFRS in India would accordingly require changes to the regulatory environment and the ability of the ICAI to move towards its planned full convergence by 2011 would be directly dependent on the pace of required regulatory change. Even though the ICAI has been gradually issuing additional accounting standards and harmonizing existing standards with IFRS, there are significant existing differences between Indian GAAP and IFRS.

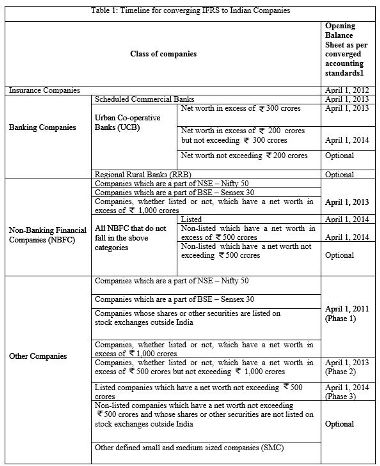

Timelines for IFRS convergence in India ::

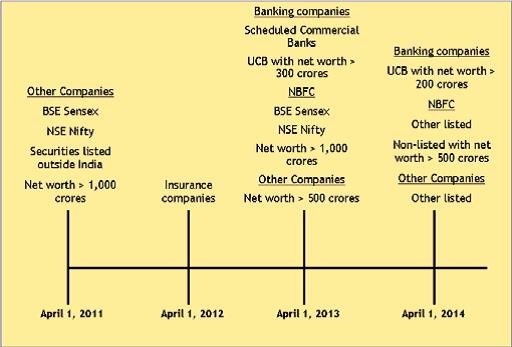

The announcements lay down a phased approach to convergence. The accounting standards which are fully convergent with IFRS will be applied in phases as set out below (Figure 1):

Figure-1

[Source: http://www.moneycontrol.com/news_html_files/news_attachment/2010/IFRS%20Roadmap%20Regulatory%20Update%20Final_1.pdf]

[Source : http: //www.moneycontrol.com/ news_html_files/ news_attachment/2010/ IFRS%20Roadmap%20Regulatory%20Update%20Final_1.pdf]

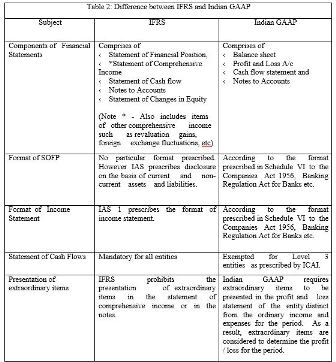

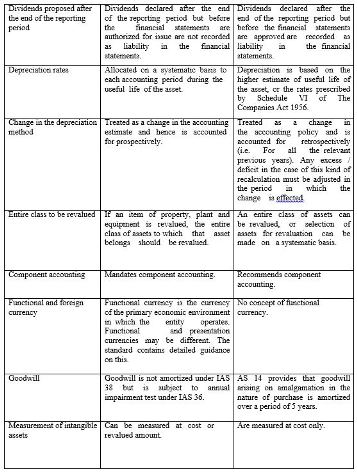

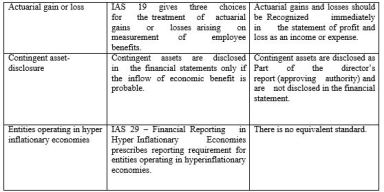

There are a number of differences between IFRS and Indian GAAP, and it would be appropriate to understand some of the qualitative as well as procedural differences between the two. An analysis of differences between Indian GAAP and IFRS is given in the table below :

[Source: www.gtgifrs.com/IFRS_Implementation_IN_India_VSP.pdf]

There are many beneficiaries of convergence with IFRS such as the economy, investors, industry and accounting professionals.

The Economy ::

As the markets expand globally the need for convergence will increases. The convergence benefits the economy by increasing growth of its international business. It facilitates maintenance of orderly and efficient capital markets and also helps to increase the capital formation and thereby economic growth. It encourages international investing and thereby leads to more foreign capital flows to the country.

Investors ::

A strong case for convergence can be made from the viewpoint of the investors who wish to invest outside their own country. Investors want the information that is more relevant, reliable, timely and comparable across the jurisdictions. Financial statements prepared using a common set of accounting standards help investors better understand investment opportunities as opposed to financial statements prepared using a different set of national accounting standards. For better understanding of financial statements, global investors have to incur more cost in terms of the time and efforts to convert the financial statements so that they can confidently compare opportunities. Investors’ confidence would be strong if accounting standards used are globally accepted. Convergence with IFRS contributes to investors’ understanding and confidence in high quality financial statements.

The Industry ::

A major force in the movement towards convergence has been the interest of the industry. The industry is able to raise capital from foreign markets at lower cost if it can create confidence in the minds of foreign investors that their financial statements comply with globally accepted accounting standards. With the diversity in accounting standards from country to country, enterprises which operate in different countries face a multitude of accounting requirements prevailing in the countries. The burden of financial reporting is lessened with convergence of accounting standards because it simplifies the process of preparing the individual and group financial statements and thereby reduces the costs of preparing the financial statements using different sets of accounting standards.

The Accounting Professionals ::

Convergence with IFRS also benefits the accounting professionals in a way that they are able to sell their services as experts in different parts of the world. The thrust of the movement towards convergence has come mainly from accountants in public practice. It offers them more opportunities in any part of the world if same accounting practices prevail throughout the world. They are able to quote IFRS to clients to give them backing for recommending certain ways of reporting. Also, for accounting professionals in industry as well as in practice, their mobility to work in different parts of the world increases.

Benefits of IFRS to Indian Corporate ::

Adopting IFRS by Indian corporate is going to be very challenging but at the same time could also be rewarding. Indian corporate is likely to reap significant benefits from adopting IFRS.

Absolute Transparency ::

IFRS will improve the comparability of financial information and financial performance with global peers and industry standards. This will result in more transparent financial reporting of a company’s activities which will benefit investors, customers and other key stakeholders in India and overseas.

World Class Peer Standards for Financial Reporting ::

The adoption of IFRS is expected to result in better quality of financial reporting due to consistent application of accounting principles and improvement in reliability of financial statements. This, in turn, will lead to increased trust and reliance placed by investors, analysts and other stakeholders. Superior financial reporting could be useful in convincing a firm’s present and potential employees of its financial soundness, so that as key users of firm’s accounting information they can trust the firm as a dependable employer. The rising use of pay for performance plans and the need for international tradability of employees stocks and stock options further underscore the need for respectable accounting rules.

Harmonization with Global Financial Market ::

Increasingly, Indian accountants and businessmen feel the need for convergence with IFRS. Capital markets provide an important explanation for this change. Some Indian companies are already listed on overseas stock exchanges and many more will list in the future. Internationally acceptable accounting standards will then become the language of communication for Indian companies. Better access to and reduction in the cost of capital raised from global capital markets since IFRS are now accepted as a financial reporting framework for companies seeking to raise funds from most capital markets across the globe. A recent decision by the US Securities and Exchange Commission (SEC) permits foreign companies listed in the US to present financial statements in accordance with IFRS. This means that such companies will not be required to prepare separate financial statements under Generally Accepted Accounting Principles in the US (US GAAP). Therefore, Indian companies listed in the US would benefit from having to prepare only a single set of IFRS compliant financial statements, and the consequent saving in financial and compliance costs. However, the perceived benefits from IFRS adoption are based on the experience of IFRS compliant countries in a period of mild economic conditions. The current decline in market confidence in India and overseas coupled with tougher economic conditions may present significant challenges to Indian companies.

Some other benefits:

- Same language

- Cross border investments leading to economic growth

- Comparability of financial statements of any two companies anywhere in the world

- Globalization of economy and world trade

- For multinational companies :

- Consolidation of group financial statements made easier

- Accounting and audit functions made easier and cheaper

- Compliance with regulatory requirements of bodies such as stock exchanges

- Mergers and acquisitions made easier

- Access to multinational funds

- The job of governments and standard setters in the developing countries made easier

- The job of tax authorities made easier

- Time and money saved by international professional accounting firms in planning and execution of accounting and audits

- Administrative costs of accessing the capital markets around the world reduced

IFRS implementation challenges in India ::

In-spite of the various benefits of adopting IFRS, implementation of IFRS is a phenomenal task in India. Following are a few challenges faced during adoption and implementation of IFRS:

- Awareness about International Practices ::

Adoption of IFRS means that the entire set of financial statements will be required to undergo a drastic change. There are a number of differences between the Indian GAAP’ and IFRS. This may cause the users of financial statements to look at them from a new perspective. It would be a challenge to bring about awareness of IFRS and its impact among the users of financial statements. - Training ::

Professional accountants are looked upon to ensure successful implementation of IFRS. The biggest hurdle for the professionals in implementing IFRS is the lack of training facilities and academic courses on IFRS in India. As the implementation date draws closer (2011), it is observed that there is acute shortage of trained IFRS staff. The solution to this problem is that all stakeholders in the organization should be trained and IFRS should be introduced as a full time subject in the universities. - Amendments to the existing law ::

It is observed that implementation of IFRS may result in a number of inconsistencies with the existing laws which include the Companies Act 1956, SEBI regulations, banking laws and regulations and the insurance laws and regulations. Currently, the reporting requirements are governed by various regulators in India and their provisions override other laws. IFRS does not recognize such overriding laws. Although steps to amend these laws have been initiated, the authorities need to ensure that the laws are amended well in time. - Taxation ::

IFRS convergence would affect most of the items in the financial statements and consequently the tax liabilities would also undergo a change. Thus the taxation laws should address the treatment of tax liabilities arising on convergence from Indian GAAP to IFRS. It is extremely important that the taxation laws recognize IFRS compliant financial statements otherwise it would duplicate administrative work for the organizations. - Fair value ::

IFRS uses fair value as a measurement base for valuing most of the items of financial statements. The use of fair value accounting can bring a lot of volatility and subjectivity to the financial statements. It also involves a lot of hard work in arriving at the fair value and valuation experts have to be used. Moreover, adjustments to fair value result in gains or losses which are reflected in the income statements. Whether this can be included in computing distributable profit is also debated. - Management Compensation Plan ::

The terms and conditions relating to management compensation plans would also have to be changed. This is because the financial results under IFRS are likely to be very different from those under the Indian GAAP. The contracts would have to be re-negotiated which is also a big challenge. - Reporting systems ::

The disclosure and reporting requirements under IFRS are completely different from the Indian reporting requirements. Companies would have to ensure that the existing business reporting model is amended to suit the reporting requirements of IFRS. The information systems should be designed to capture new requirements related to fixed assets, segment disclosures, related party transactions, etc. Existence of proper internal control and minimizing the risk of business disruption should be taken care of while modifying or changing the information systems.

Convergence to IFRS will greatly enhance an Indian entities’ ability to raise and attract foreign capital at a low cost. A common accounting language, such as IFRS, will help Indian companies benchmark their performance with global counterparts. Early adoption of IFRS gives companies the opportunity to anticipate challenges, manage outcomes and implement the best solutions. Without careful study, the full impact of converting to IFRS will not be clear. Companies need to conduct a diagnostic study before proceeding for a full IFRS conversion. After completing the preliminary assessment, the management should prepare a detailed IFRS conversion program. Given the enormity of the exercise, companies should consider a dedicated team that will work on the conversion exercise. For successful implementation of IFRS in India, the regulator should immediately announce its intention to convert to IFRS and make appropriate regulatory amendments.

REFERENCES :

***************************************************

Dr. Pravin R. Patel

Incharge Principal

Gujarat Commerce College

Ahmedabad

EMail ID : prof.prpatel@yahoo.co.in

Home | Archive | Advisory Committee | Contact us