LEAN ACCOUNTING-AN EMERGING CONCEPT

ABSTRACT::

With many manufacturers now undergoing a lean transformation, it becomes essential to discover exactly what part lean accounting has played in the changes made. Surprisingly, this is still an emerging concept. Reasons ranged from a lack of understanding to the barrier of company culture. This paper will cut through some of the common misconceptions about lean accounting and lean management.

KEY WORDS::

Lean accounting, Lean manufacturing, Value stream, Lean management, Operation Principles

Introduction::

Since 1990, the 'lean thinking basis' was introduced. The main start point is value, which states that the organization Resources should focus on activities that lead to making value for all beneficiary people and also omit the losing additional value group and include parallel activities in the organization. . (Kim Loader 2010)

Value determination dimensions take place in the value flow. Value flow is a set of all necessary activities for a certain product that include all production and services processes, i.e. from the sketch to the advent of the products and services to the market. ( Emiliani, Bob2007)

The term 'lean production' was developed by Toyota Company. The executive managers of Toyota state that they inspired this famous system through a visit of Motor Ford Company and then developed that and they owe this to endeavors of managers like Taichi and Ohno and his consultant Shijo Shinko. In the late 1980 the Americans and the Europeans acknowledged this system. (Emiliani, Bob (March 23, 2007))

Lean accounting is looking forward decreasing the stages in implementation process and omitting the standard prices for achieving real prices and inhibiting expense allotments, whereas lean control operations are still considering measurement of system performance and emphasize on social and behavioral controls.

There are two main forces for lean accounting. First is implementing lean methods for accounting, control and processing in companies. Here the goal is to increase the speed of the process and to omit the waste, unusable capacity, errors and defects.

Second is that lean accounting should basically change the process of accounting, control and measurement so that it causes lean change and improves information and provides information that is suitable for decision making, and this information rely on the customer keeping principle (Maskell, & Baggaley, 2004)

The reasons of need to lean accounting:

Like most lean methods, lean accounting is in fact provided and developed for supporting production companies and most of the implementation of lean accounting is seen in production companies. But nowadays lean methods have entered the other industries like financial services, sanitary, remedy and caretaking centers, government and Training, so lean accounting should also exist in these industries but there is no reported case about utilizing lean accounting out of the production section. (Fiume & Cunningham (March 25, 2003)

Operation principles and lean accounting tools:

KEY FEATURES OF LEAN MANAGEMENT

Lean Accounting is actually the cornerstone of a completely different model of manufacturing management – an entirely different business model. By itself, Lean Accounting has limited value, but as the financial basis for the architecture and application of logistics, quality management, factory operations, marketing and pricing, and other critical business functions, Lean Accounting is extraordinarily powerful.

A core principle of Lean Accounting is that the Value Stream is the only appropriate cost collection entity within the organization, as opposed to traditional accounting’s use of cells, cost or profit centers or departments normally based on smaller, functional groupings of work activity. The core idea behind lean is minimising waste, therefore creating more value for customers with fewer resources.

The value stream is the complete sequence of activities within the organization that operationally links the incoming supply chain with one or more outgoing distribution channels, as well as the complete sequence of associated business activities required to take a customer order from start to finish. Only by assessing financial impact in the Value Streamstructure can management be assured that a dollar saved at some point in the process did not trigger two dollars to be spent elsewhere.

Lean manufacturing is thus a continuous way of producing what the customer wants, when they want it, at a price they are prepared to pay and using the least amount of resources.

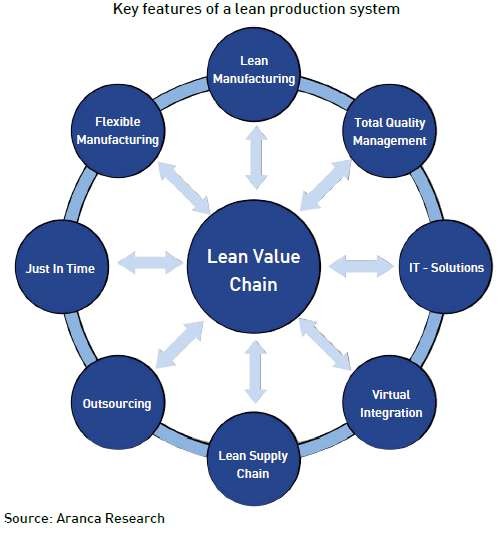

There are several potential areas in a production chain, where an organization can eliminate waste by going lean. For example, using production equipment up to the maximum potential can significantly help reduce waste. Similarly, low-cost automation is another area that can cut costs. On the sourcing side, purchasing standard parts and re using parts by dismantling old machines can also assist in waste reduction. The key features of a lean production system are depicted in the figure below:

There are positive and negative reasons for using Lean Accounting. The positive reasons are detailed below:

WHY IS TRADITIONAL ACCOUNTING NOT NEEDED?

The negative reasons for using Lean Accounting lie with the inadequacy of traditional accounting systems to support a lean culture. Everybody working seriously on the lean transformation of their company eventually bumps up against their accounting systems. Traditional accounting systems (particularly those using standard costing, activity-based costing, or other full absorption methods) are designed to support traditional management methods. As a company moves to lean thinking, many of the fundamentals of its management system change and traditional accounting, control, and measurement methods become unsuitable. Some examples of this are:

The methods of Lean Accounting are new ideas. They are mostly adaptations of methods that have been used for many years, and have been codified into a Lean Management System designed to support the needs of lean thinking organizations.

CONVERSION TO LEAN ACCOUNTING

The transition from traditional management – from a functional organizational structure and traditional accounting to Value Streams and Lean Accounting – is best viewed as an ongoing process, rather than a project. The transition from the old structures to the new can be lengthy and difficult. Often firms have expensive, major pieces of equipment, such as paint systems, heat treat equipment or other „monument‟ equipment that must be shared across two or more Value Streams. Such sharing necessitates continuing to allocate the costs of the equipment until such a time as it can be economically replaced with smaller, dedicated machines in each Value Stream.

Similarly, human resources may need to be shared until sufficient cross training can be accomplished. An example might be a company with one buyer and two schedulers that is converting to three Value Streams. The buyer and schedulers will have to be cross trained into three buyer-schedulers, each handling both the buying and the scheduling in a Value Stream.

Finally, management may choose to limit the resources put into the Value Streams until the Value Stream management has climbed the necessary learning curve and can handle some of the more difficult and critical functions. Examples might include new product development or supplier selection, which management may want to keep out of the Value Streams and in their functional area for a matter of months or even years until the Value Streams can manage them effectively.

While the transition is taking place there will be shared resources and shared people, and a degree of allocation of the expenses to the Value Streams will be necessary. This is entire normal and reasonable. Each dedicated resource and each expense that can be directly charged to a Value Stream is a step toward greater accuracy. All that is required is a dedication to continually increasing the resources in the organization assigned directly to Value Streams and continually reducing the percentage of expenses allocated and correspondingly increasing the direct expenses to the Value Streams.

REFERENCES

***************************************************

Dr Gurudutta P Japee Dr Bhavesh A Lakhani

Gujarat Commerce College

Ahmedabad

Shri K.Ka Shastri Government Commerce College

Ahmedabad

Home | Archive | Advisory Committee | Contact us