E-Banking: Opportunities and Threats

Introduction ::

Features & Advantages of E-banking:

Internet banking is changing the banking industry and is having the major effects on banking relationships. Banking is now no longer confined to the branches where one has to approach the branch in person, to withdraw cash or deposit a cheque or request a statement of accounts. In true Internet banking, any inquiry or transaction is processed online without any reference to the branch (anywhere banking) at any time. Providing Internet banking is increasingly becoming a "need to have" than a "nice to have" service. Internet banks have lower operational and transactional costs than do traditional walled banks. Internet banking is not limited to a physical site; some Internet banks exist without physical branches, for example Banknet (UK).

The basic on-line activity is paying bills. Swedbank was the first bank in the world to introduce “Electronic Bill Presentment and Payment (EBPP)” and now handles more than 4 million bill payments a month.Top of Form

Several studies have pointed to the fact that the cost of delivery of banking service through Internet is several times less than the traditional delivery methods. This alone is enough reason for banks to flock to Internet and to deliver more and more of their services through Internet. Not adopting this new technology in time has the risk of banks getting edged out of competition. In India, too e-banking has taken roots. Almost all the private and public sector banks have set up banking portals allowing their customers to access facilities like obtaining information, querying on their accounts, etc. Soon, still higher level of online services will be made available.

At present, the total Internet users in the country are estimated at 10 crores. However, this is expected to grow exponentially to 20 crores by 2020. Only about 1% of Internet users did banking online in 1998. This increased to 16.7% in March 2000 and increased to 38.6% in 2010 while at present around 40% internet users doing Net banking. (idc report) The growth potential is, therefore, immense. Further incentives provided by banks would discourage customers from visiting physical branches.

"Use of the Internet for banking has seen a massive rise in the 2010-11 survey, taking the overall number of bank consumers who use the Net to close 7% of the total bank account holders -- a seven-fold jump since 2007 -- even as for the first time in the past 13 years, branch banking has come down by a full 15 percentage points during the same period," McKinsey & Company India partner and head of its retail banking services Renny Thomas said.

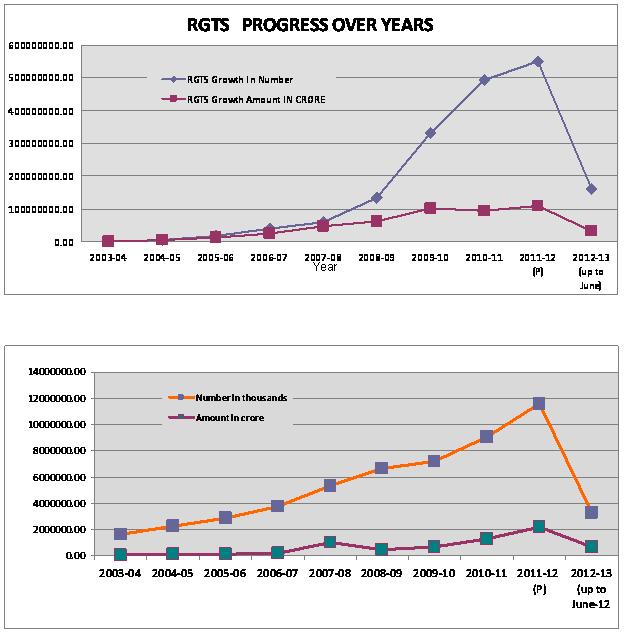

Below graphs indicate the growth in RGTS and NEFT over the years (source: RBI monthly data)

Some of the distinctive features of e-banking are:

Advantage of Internet banking

OPENING AN ACCOUNT:

Customers, who have existing accounts at their Physical banks and want to begin using electronic banking services, may simply apply to their Bank for a password for Internet banking. Once they have joined the system, customers have electronic access to all of their accounts at the bank some banks providing Net banking password hand to hand. (eg. SBI).The banks providing Internet banking service, at present are only willing to accept the request for opening of accounts. The accounts are opened only after proper physical introduction and verification. This is primarily for the purpose of proper identification of the customer and also to avoid “benami accounts” as also money laundering activities that might be undertaken by the customer. Supervisors world over, expect the Internet banks also to follow the practice of ‘know your customer’ (KYC).

Services availed through E-Banking.

Bill payment service

One can facilitate payment of electricity and telephone bills, mobile phone, credit card and insurance premium bills as each bank has tie-ups with various utility companies, service providers and insurance companies, across the country. To pay the bills, one has need to do is complete a simple one-time registration for each biller. You can also set up standing instructions online to pay your recurring bills, automatically. Generally, the bank does not charge customers for online bill payment.

Fund Transfer

One can transfer any amount from one account to another of the same or any another bank. Customers can send money anywhere in India. Once you login to your account, you need to mention the payees's account number, his bank and the branch. The transfer will take place in a day or so, whereas in a traditional method, it takes not less than three working days.

Credit card customers

With Internet banking, customers can not only pay their credit card bills online but also get a loan on their cards. If you lose your credit card, you can report lost card online.

Railway pass , Railway and Air Ticket booking

This is something that is in the interest all the aam janta. Indian Railways has tied up with some premier banks and one can now make his/her railway pass for local trains online. The pass will be delivered at ones doorstep.

Investing through Internet banking

One can now open FD/RD account online through funds transfer. Investors with interlinked demat account and bank account can easily trade in the stock market and the amount will be automatically debited from their respective bank accounts and the shares will be credited in their demat account. Moreover, now banks even give the facility to purchase mutual funds and bonds directly from the online banking system.

Recharging prepaid phone

Now just top-up prepaid mobile cards by logging in to Internet banking. By just selecting his/her operator's name, entering mobile number and the amount for recharge, ones phone is again back in action within few minutes.

Shopping

With a range of all kind of products, one can shop online and the payment is also made conveniently through his/her account.

Donations

One can made donations to famous siddhivinayaka or Tirupati balaji or Shirdi’s Sai Baba temples or can make donations on line to various NGO’s etc.

Risks, Issues & Security Precautions:

Operational risk, also referred to as transactional risk is the most common form of risk associated with e-banking. It takes the form of inaccurate processing of transactions, non enforceability of contracts, compromises in data integrity, data privacy and confidentiality, unauthorized access / intrusion to bank’s systems and transactions etc. Such risks can arise out of weaknesses in design, implementation and monitoring of banks’ information system. Besides inadequacies in technology, human factors like negligence by customers and employees, fraudulent activity of employees and crackers / hackers etc. can become potential source of operational risk. Often there is thin line of difference between operational risk and security risk and both terminologies are used interchangeably.

Internet banking frauds:

The Internet is in the public domain whereby geographical boundaries are eliminated. Cyber crimes are therefore difficult to be identified and controlled. In order to promote Internet banking services, it is necessary that the proper legal infrastructure is in place. Government has introduced the Information Technology Bill, which has already been notified in October 2000. Section 72 of the Information Technology Act, 2000 casts an obligation of confidentiality against disclosure of any electronic record, register, correspondence and information, except for certain purposes and violation of this provision is a criminal offence.

Phishing:

A person's personal details are obtained by fraudsters posing as bankers, who float a site similar to that of the person's bank. They are asked to provide all personal information about themselves and their account to the bank on the pretext of database up-gradation. The number and password are then used to carry out transactions on their behalf without heir knowledge. Typically, a phishing email will ask an online banking customer to follow a link in order to update personal bank account details. If the link is followed, the victim downloads a program which captures his or her banking login details and sends them to a third party

Key Challenges & Conclusion

Banking is essentially an art of managing people, be it customers or staff. In a competitive environment, customers have to be treated as kings. Thus, delivering financial services to the satisfaction of customer, and prompt redressal of complaints of customers, if any, are very important. The bankers should also take pro-active actions to increase customer awareness with regard to charges applicable to the financial services and the available redressal mechanisms. It also has to be ensured that the products cover all segments of the population and provide an incentive to adopt these products. The regulatory process would support all orderly development of new systems and processes, within the legal mandate. Hope this Conference will deliberate on all these issues especially how the aam aadmi can be provided cost-effective, safe, speedier and hassle free payment and settlement products and solutions. Thus, in sum, banking affects all of us. Our lives are dependent on the banking sector in one way or another, directly or indirectly. It is the life-blood of the economy, a contamination of the same can affect any sector or region of the economy. The challenge before all the stakeholders including banks and non-bank players, IT vendors, other service providers, etc. is how to introduce such a next generation payment and settlement system and solutions that is needed to take the country into the golden era of 21st century. This time, it is worth to recall the slogan given by Hon CM of Gujarat shri Narendra Modi: IT + IT = IT (Information Technology + Indian Talent = India Tomorrow).

REFERENCES :

***************************************************

Dr.Meenakshi Somani

M.Com., Ph.D., PGD(Yoga)

734-B-1, Vastunirman Society, Sector 22,

Gandhinagar-382024

9427306536 / 079-23240809

Somaniminaxi@Gmail.Com

Home | Archive | Advisory Committee | Contact us