Transfer Pricing - A Road Ahead

Abstract ::

We have studied the various dimensions of transfer pricing such as base of transfer pricing, external and internal reasons effects to transfer pricing ,over & under invoicing by way of transfer pricing, transfer pricing manipulations, transfer pricing effects etc. The study of transfer pricing covers how accounting profit can be changed for the purpose of saving the tax with the help of various types of policies adopted by the organization, e.g. revenue policy, sales tax policy ,vat policy etc. Transfer pricing refers to the pricing of goods and services within a multi-divisional organization. Goods from the production division may be sold to the marketing division or goods from a parent company may be sold to a foreign subsidiary.

The study includes the rules & regulations for transfer pricing transactions for goods & services with each other. The terms related with transfer pricing method such as Divisional Transfer Pricing, Market Price Transfer Pricing, Dual Transfer Pricing, Nationalised Transfer Pricing, etc. are also explained.

At last transfer pricing is explained by diagram which shows that how the transfer price is decided with the help of optimum production level, marginal revenue, marginal cost. This effect is cleared in the following three markets: (A)With No External Market, (B)With Competitive External Market and (C)With Imperfect External Market. In this paper we have try to cover multiple dimensions of transfer pricing.

Key Words:-Pricing, Dual Transfer, Transactional Profit Method, Negotiated Price

Introduction ::

A transfer price is the notional value placed on goods and services transfer from one division to another within a large business organization. Some companies have the problem of pricing goods and services which are transferred to other divisions of the same company, such pricing is referred to as intracomany, inter divisional or transfer pricing.

Definition

Price charged by individual entities for goods or services supplied to one another in multi-department, multi-office, or multinational firms. Transfer price policy is generally aimed at (1) Evaluating financial performance of different business units (profit centers) of a conglomerate, and/or to and (2) Shift earnings from a high tax jurisdiction to a low-tax one. Tax authorities usually frown upon transfer pricing aimed at tax avoidance and insist that each internal part of the firm deals with the other on 'arm's length' (market price) basis. Also called transfer cost.

Transfer price is in the Accounting & Auditing and Economics, Politics, Society subjects.

Transfer price appears in the definitions of the following terms: transfer cost, up streaming, unitary tax system (UTS) and market price

Arm’s Length Price (ALP) – This is the price that would be charged in uncontrollable transactions, i.e. when parties are unrelated. Two most common methods of doing this are

1. Checking the price in a similar transaction between two totally different parties and

a) Comparable uncontrolled price method (CUP)

b) Resale price method (RPM)

c) Cost plus method (CPM)

d) Profit split method (PSM)

e) Transactional Profit Method (TPM)

f) Transactional net margin method (TNM)

g) Such other method as may be prescribed by the Board.

Transfer Pricing Methods

Comparable Uncontrolled Price Method

The CUP method provides the best evidence of an arm's length price. A CUP may arise where: the taxpayer or another member of the group sells the particular product, in similar quantities and under similar terms to arm's length parties in similar markets (an internal comparable);

an arm's length party sells the particular product, in similar quantities and under similar terms to another arm's length party in similar markets (an external comparable); the taxpayer or another member of the group buys the particular product, in similar quantities and under similar terms from arm's length parties in similar markets (an internal comparable); or an arm's length party buys the particular product, in similar quantities and under similar terms from another arm's length party in similar markets (an external comparable).

Where differences exist between controlled and uncontrolled transactions, it may be difficult to determine the adjustments necessary to eliminate the effect on transfer prices. However, the difficulties that arise in making adjustments should not routinely preclude the potential application of the CUP method. Therefore, taxpayers should make reasonable efforts to adjust for differences.

Resale price method of Transfer Pricing

The resale price method begins with the resale price to arm's length parties (of a product purchased from an non-arm's length enterprise), reduced by a comparable gross margin. This comparable gross margin is determined by reference to either the resale price margin earned by a member of the group in comparable uncontrolled transactions (internal comparable) or the resale price margin earned by an arm's length enterprise in comparable uncontrolled transactions (external comparable).

Under this method, the arm's length price of goods acquired by a taxpayer in a non-arm's length transaction is determined by reducing the price realized on the resale of the goods by the taxpayer to an arm's length party, by an appropriate gross margin. This gross margin, the resale margin, should allow the seller to Recover its operating costs; and earn an arm's length profit based on the functions performed, assets used, and the risks assumed.

Where the transactions are not comparable in all ways and the differences have a material effect on price, the taxpayer must make adjustments to eliminate the effect of those differences. The more comparable the functions, risks and assets, the more likely that the resale price method will produce an appropriate estimate of an arm's length result.

An exclusive right to resell goods will usually be reflected in the resale margin. The resale price method is most appropriate in a situation where the seller adds relatively little value to the goods. The greater the value-added to the goods by the functions performed by the seller, the more difficult it will be to determine an appropriate resale margin. This is especially true in a situation where the seller contributes to the creation or maintenance of an intangible property, such as a marketing intangible, in its activities.

Cost plus method of Transfer Pricing

The cost plus method begins with the costs incurred by a supplier of a product or service provided to an non-arm's length enterprise, and a comparable gross mark-up is then added to those costs. This comparable gross mark-up is determined in two ways, by reference to the cost plus mark-up earned by a member of the group in comparable uncontrolled transactions (internal comparable) or the cost plus mark-up earned by an arm's length enterprise in comparable uncontrolled transactions (external comparable).

In either case, the returns used to determine an arm's length mark-up must be those earned by persons performing similar functions and preferably selling similar goods to arm's length parties. Where the transactions are not comparable in all ways and the differences have a material effect on price, taxpayers must make adjustments to eliminate the effect of those differences, such as differences in the relative efficiency of the supplier; and any advantage that the activity creates for the group.

The more comparable the functions, risks and assets, the more likely it is that the cost plus method will produce an appropriate estimate of an arm's length result.

In general, for purposes of applying a cost-based method, costs are divided into three categories:

The cost plus method uses margins calculated after direct and indirect costs of production. In comparison, net margin methods-such as the transactional net margin method (TNMM) discussed in Section B of this Part-use margins calculated after direct, indirect, and operating expenses. For purposes of calculating the cost base for the net margin methods, operating expenses usually exclude interest expense and taxes.

Properly determining cost under the cost plus method is important. Cost is usually calculated in accordance with accounting principles that are generally accepted for that particular industry in the country where the goods are produced.

However, it is most important that the cost base of the transaction of the tested party to which a mark-up is to be applied be calculated in the same manner as-and reflects similar functions, risks, and assets as-the cost base of the comparable transactions. Where cost is not accurately determined in the same manner, both the mark-up (which is a percentage of cost) and the transfer price (which is the total of the cost and the mark-up) will be misstated.

For example, if the comparable party includes a particular item as an operating expense, while the tested party includes the item in its cost of goods sold, the cost base of the comparable must be adjusted to include the item.

Profit split method of Transfer Pricing ::

Under the profit split method::

The first step is to determine the total profit earned by the parties from a controlled transaction. The profit split method allocates the total integrated profits related to a controlled transaction, not the total profits of the group as a whole. The profit to be split is generally the operating profit, before the deduction of interest and taxes. In some cases, it may be appropriate to split the gross profit.

The second step is to split the profit between the parties based on the relative value of their contributions to the non-arm's length transactions, considering the functions performed, the assets used, and the risks assumed by each non-arm's length party, in relation to what arm's length parties would have received.

The profit split method may be applied where the operations of two or more non-arm's length parties are highly integrated, making it difficult to evaluate their transactions on an individual basis; and the existence of valuable and unique intangibles makes it impossible to establish the proper level of comparability with uncontrolled transactions to apply a one-sided method.

Due to the complexity of multinational operations, one member of the multinational group is seldom entitled to the total return attributable to the valuable or unique assets, such as intangibles.

Also, arm's length parties would not usually incur additional costs and risks to obtain the rights to use intangible properties unless they expected to share in the potential profits. When intangibles are present and no quality comparable data are available to apply the one-sided methods (i.e., cost plus method, resale price method, the TNMM), taxpayers should consider the use of a profit split method.

The second step of the profit split method can be applied in numerous ways, including:

splitting profits based on a residual analysis; and relying entirely on a contribution analysis.

Following the determination of the total profit to be split in the first step of the profit split, a residual profit split is performed in two stages. The stages can be applied in numerous ways, for example:

Stage 1: The allocation of a return to each party for the readily identifiable functions (e.g., manufacturing or distribution) is based on routine returns established from comparable data. The returns to these functions will, generally, not account for the return attributable to valuable or unique intangible property used or developed by the parties. The calculation of these routine returns is usually calculated by applying the traditional transaction methods, although it may also involve the application of the TNMM.

Stage 2: The return attributable to the intangible property is established by allocating the residual profit (or loss) between the parties based on the relative contributions of the parties, giving consideration to any information available that indicates how arm's length parties would divide the profit or loss in similar circumstances.

Transactional Profit Methods of Transfer Pricing ::

Traditional transaction methods are the most reliable means of establishing arm's length prices or allocations. However, the complexity of modern business situations may make it difficult to apply these methods. Where the information available on comparable transactions is not detailed enough to allow for adjustments necessary to achieve comparability in the application of a traditional transaction method, taxpayers may have to consider transactional profit methods.

However, the transactional profit methods should not be applied simply because of the difficulties in obtaining or adjusting information on comparable transactions, for purposes of applying the traditional transaction methods. The same factors that led to the conclusion that it is not possible to apply a traditional transaction method must be considered when evaluating the reliability of a transactional profit method.

Transactional net margin method (TNMM)::

The key difference between the profit split method and the TNMM is that the profit split method is applied to all members involved in the controlled transaction, whereas the TNMM is applied to only one member.

The more uncertainty associated with the comparability analysis, the more likely it is that a one-sided analysis, such as the TNMM, will produce an inappropriate result. As with the cost plus and resale price methods, the TNMM is less likely to produce reliable results where the tested party contributes to valuable or unique intangible assets. Where uncertainty exists with comparability, it may be appropriate to use a profit split method to confirm the results obtained.

The TNMM compares the net profit margin of a taxpayer arising from a non-arm's length transaction with the net profit margins realized by arm's length parties from similar transactions; and examines the net profit margin relative to an appropriate base such as costs, sales or assets.

This differs from the cost plus and resale price methods that compare gross profit margins. However, the TNMM requires a level of comparability similar to that required for the application of the cost plus and resale price methods. Where the relevant information exists at the gross margin level, taxpayers should apply the cost plus or resale price method.

Because the TNMM is a one-sided method, it is usually applied to the least complex party that does not contribute to valuable or unique intangible assets. Since TNMM measures the relationship between net profit and an appropriate base such as sales, costs, or assets employed, it is important to choose the appropriate base taking into account the nature of the business activity. The appropriate base that profits should be measured against will depend on the facts and circumstances of each case.

Barriers of Traditional Transfer Price::

Managers considered but reject several traditional methods for establishing a new transfer pricing system:

Market price

Full cost,

Marginal cost,

and negotiated price.

Market price for the transferred product is not feasible if no market is existed for any manufacturing company’s products which is not distributed or marketed to customers. A full cost calculation including materials, labor, and manufacturing overhead is rejected because the traditional methods for allocating overhead (labor or machine hours) does not capture the actual cost structure. Also, the accumulation of all factory costs into average overhead rates could encourage local optimization by each division that would lower company’s overall profit. For example, manufacturing plants would be encouraged to overproduce in order to absorb more factories overhead into inventory, while marketing divisions might be discouraged from bidding aggressively for high-volume orders and encouraged to accept more low-volume custom orders. Also, this system would not reveal the incremental costs associated with short-run decisions or the relative use of capacity by different products and different order sizes.

Using short-run marginal cost, covering only ingredients and packaging materials, was the system proposed initially, which the managers already knew was inadequate for their purposes. And, finally, senior executives believed strongly that negotiated transfer prices would lead to endless arguments among managers in the different divisions, which would consume excessive time on nonproductive discussions.

TRANSFER PRICING MANIPULATIONS::

Above reasons leads to the point of Transfer Pricing Manipulations (TPM).It is TPM that is discouraged by Government as against Transfer Pricing which is the act of pricing. However, in common parlance, it is Transfer Pricing which generally used to mean TPM.

TPM is fixing transfer price on non-market basis which generally results in saving the total quantum of organisation’s tax by shifting accounting profits from high tax to low tax jurisdictions. The implication is moving of one nation’s tax revenue to another. A similar phenomenon exists in domestic markets where different states attract investment by under cutting Sales tax rates, leading to outflow from one state to another, something the government is trying to curb by way of implementations of VAT.

MOTIVATION FOR TPM::

It is not just the corporate tax deferential that includes organizations to manipulations in transfer pricing. Some of the other reasons are :

High Custom Duty-leading to under-invoicing of goods.

Restriction on Profit Repatriation- leading to over-invoicing of raw materials etc. transferred from parent country, hence compensating for locked forex.

Ownership Restrictions (E.g. insurance sector-26% )- since this leads to less than justified returns on the technology or knowledge invested in the JV,MNEs circumvent it through over charging on royalties for technology, etc.

There can be various other similar motivations for TPM. The transactions most likely disputed by Government are Administration & Management Fees, Royalties for intangibles and transfer of finished goods for resale.(source &Y Survey).

EFFECTS OF TPM ON NATIONS::

One primary and well appreciated effect is the loss of Government Tax and Custom Duty revenues. Loss of tax revenues in this form leads to a burden on the rest of the population through over taxation and/or borrowings by the Government, which becomes essential to meet expenditure requirements.

TPM also leads to distortions in Balance of Payments between the host and home country, something that has the potential to challenge the sovereignty of nations given the mega size of some of these firms. Another implication is on the location of international production and employment. Given the objective of maximization of global profits, MNEs will open subsidiaries where production is most profitable, which is where tax burden is less and therefore effect the level of FDI a country gets. This linkage is so strong that some like Hong Kong and Singapore have no Transfer Pricing controls, making themselves attractive destinations for FDI.

Transfer pricing has been existing in domestic and importantly international transactions over decades now and there is nothing novel about the concept. What is, however, is the extent of this practice which has now acquired critical mass to be given due consideration by various tax authorities.

TPM GAINING IMPORTANCE::

The issue has gained importance in the recent past due to organizations acquiring huge economic power (in some cases more than nations themselves - Of the 100 biggest economies, 51 are companies and 49 are countries) operating in scores of nations, making their sales, production and distribution structure more and more complex to come under the purview of one tax regime.

The other phenomenon is increasing liberalization due to which a larger number of countries are allowing entry of these MNEs and a further larger number making their environment conducive for foreign investment. This has led to establishment of truly global corporations resulting in a higher proportion of intra organization trade in international trade. To substantiate the idea further, one-thirds of total world trade is intra-firm.

A third phenomenon, particularly in countries like India, is one of Government moving away from control of productive resources (by way of divestment, etc.) which has put all the more emphasis on tax revenues in meeting Govt.’s revenue requirements.

CHECKING TRANSFER PRICING MANIPULATION::

Having understood the implications and growing importance of Transfer Pricing, more precisely Transfer Pricing Manipulation, we look at what regulations have been enacted to counter this by India.

TRANSFER PRICING DOCUMENTATION

An increasing number of countries now impose transfer pricing documentation requirements, most of which can be onerous for affected businesses. Using finely tuned methods to efficiently document transfer pricing policies, dedicated specialists—including economists and tax professionals—can provide an integrated, multi-country approach to meeting documentation obligations.

The DECOSIMO Global Transfer Pricing Team, comprised of dedicated transfer pricing specialists with advanced training in economics, accounting, project management and law, will work with you to develop a strategy to meet your global business goals and objectives.

Transfer Pricing in Different Market situation

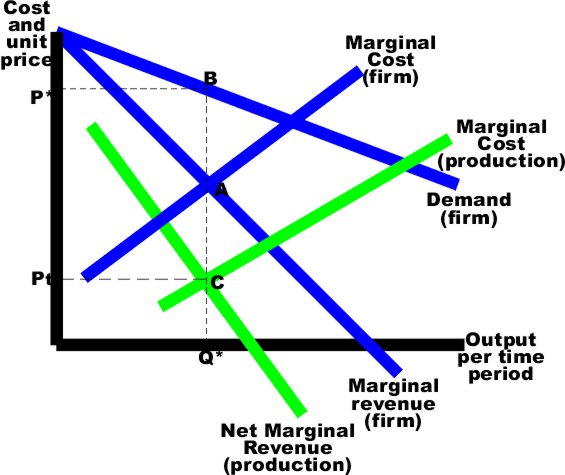

The choice of the transfer prices affects the division of the total profit among the parts of the company. It can be advantageous to choose them such that, in terms of bookkeeping, most of the profit is made in a country with low taxes. From marginal price determination theory, we know that generally the optimum level of output is that where marginal costs equals marginal revenue.

That is to say, a firm should expand its output as long as the marginal revenue from additional sales is greater than their marginal costs. In the diagram that follows, this intersection is represented by point A, which will yield a price of P*, given the demand at point B.

When a firm is selling some of its product to itself, and only to itself (i.e.: there is no external market for that particular transfer good), then the picture gets more complicated, but the outcome remains the same. The demand curve remains the same. The optimum price and quantity remain the same. But marginal cost of production can be separated from the firms’ total marginal costs. Likewise, the marginal revenue associated with the production division can be separated from the marginal revenue for the total firm. This is referred to as the Net Marginal Revenue in production (NMR), and is calculated as the marginal revenue from the firm minus the marginal costs of distribution.

It can be shown algebraically that the intersection of the firms marginal cost curve and marginal revenue curve (point A) must occur at the same quantity as the intersection of the production divisions marginal cost curve with the net marginal revenue from production (point C).

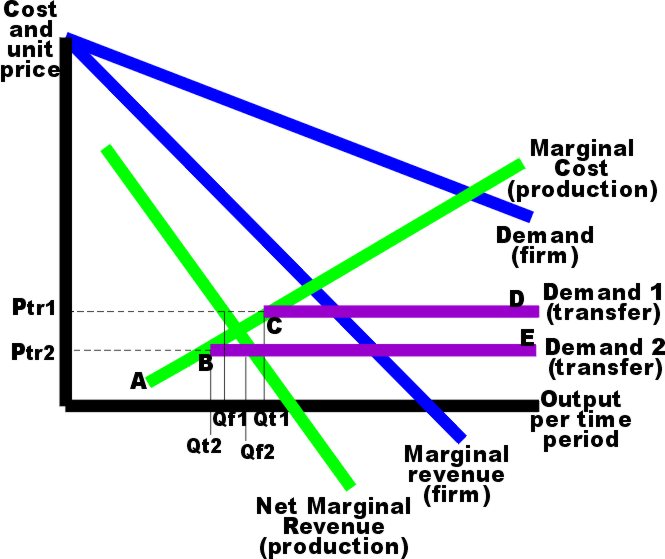

If the production division is able to sell the transfer good in a competitive market (as well as internally), then again both must operate where their marginal costs equal their marginal revenue, for profit maximization. Because the external market is competitive, the firm is a price taker and must accept the transfer price determined by market forces (their marginal revenue from transfer and demand for transfer products becomes the transfer price). If the market price is relatively high (as in Ptr1 in the next diagram), then the firm will experience an internal surplus (excess internal supply) equal to the amount Qt1 minus Qf1. The actual marginal cost curve is defined by points A,C,D.

If the market price is relatively low (as in Ptr2), then the firm will experience an internal shortages (insufficient internal supply) equal to the amount Qf2 minus Qt2. The actual marginal cost curve is defined by points A,B,E.

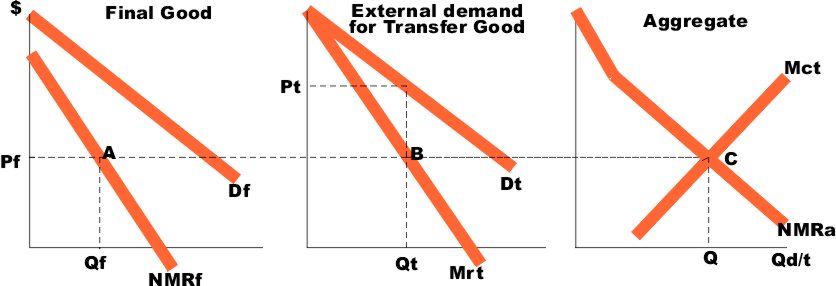

If the firm is able to sell its transfer goods in an imperfect market, then it need not be a price taker. There are two markets each with its own price (Pf and Pt in the next diagram). The aggregate market is constructed from the first two. That is, point C is a horizontal summation of points A and B (and likewise for all other points on the Net Marginal Revenue curve (NMRa). The total optimum quantity (Q) is the sum of Qf plus Qt.

REFERENCES :

***************************************************

Dr. Bhavesh Lakhani

Faculty of Commerce,

Shri K.Ka. Shahstri Govt. Commerce College,

Maninagar, Ahmedabad-8

proflakhani@yahoo.com

Dr. Gurudutta Japee,

Faculty of Accountancy,

S.M. Patel Institute of Commerce,

Ahmedabad-6

profgurudutta@gmail.com

Home | Archive | Advisory Committee | Contact us